Carbon Credit ETF Overview | KRBN & KCCA | KraneShares

by Kraneshares

KraneShares Carbon Suite:

Investing in the Global Carbon Allowance Markets

KRBN

KCCA

3/31/2026

Introduction to KraneShares

About KraneShares

Krane Funds Advisors, LLC is a specialist investment manager focused on China, Carbon, Climate, and other uncorrelated assets. KraneShares seeks to provide innovative, high conviction, and first to market strategies. The firm was founded in 2013 and manages for institutions and individuals globally. In 2017, KraneShares formed a strategic partnership with China International Capital Corporation (CICC) when they acquired a majority ownership stake. The firm is a signatory of the United Nations-supported Principles for Responsible Investment (UN PRI).

Sign up to our weekly carbon market blog: www.climatemarketnow.com

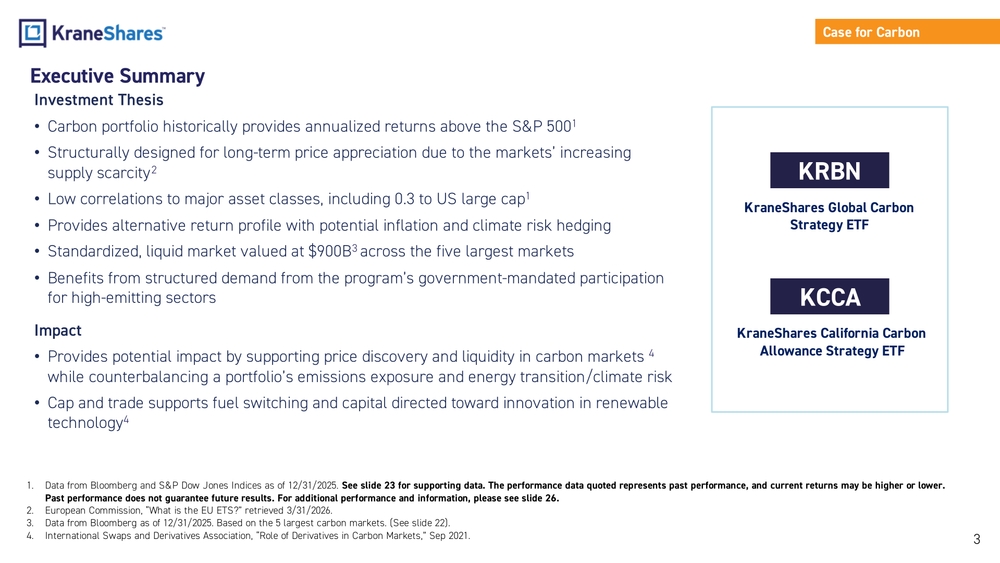

Executive Summary

Investment Thesis

- Carbon portfolio historically provides annualized returns above the S&P 500

- Structurally designed for long-term price appreciation due to the markets' increasing supply scarcity

- Low correlations to major asset classes, including 0.3 to US large cap

- Provides alternative return profile with potential inflation and climate risk hedging

- Standardized, liquid market valued at $900B across the five largest markets

- Benefits from structured demand from the program's government-mandated participation for high-emitting sectors

Impact

- Provides potential impact by supporting price discovery and liquidity in carbon markets while counterbalancing a portfolio's emissions exposure and energy transition/climate risk

- Cap and trade supports fuel switching and capital directed toward innovation in renewable technology

KRBN — KraneShares Global Carbon Strategy ETF

KCCA — KraneShares California Carbon Allowance Strategy ETF

Growing Institutional Interest

CFA Institute Research & Policy Center

Global Compliance Carbon Markets: Structure Explained — Yushuo Yang, CFA

Cambridge Associates

Are California Carbon Allowances an Attractive Investment?

#1 New Release in Sustainable Business Development

Carbon Hunters: Reflections and Forecasts of Climate Markets in the 21st Century — Richard Sandor, Paula DiPerna (World Scientific)

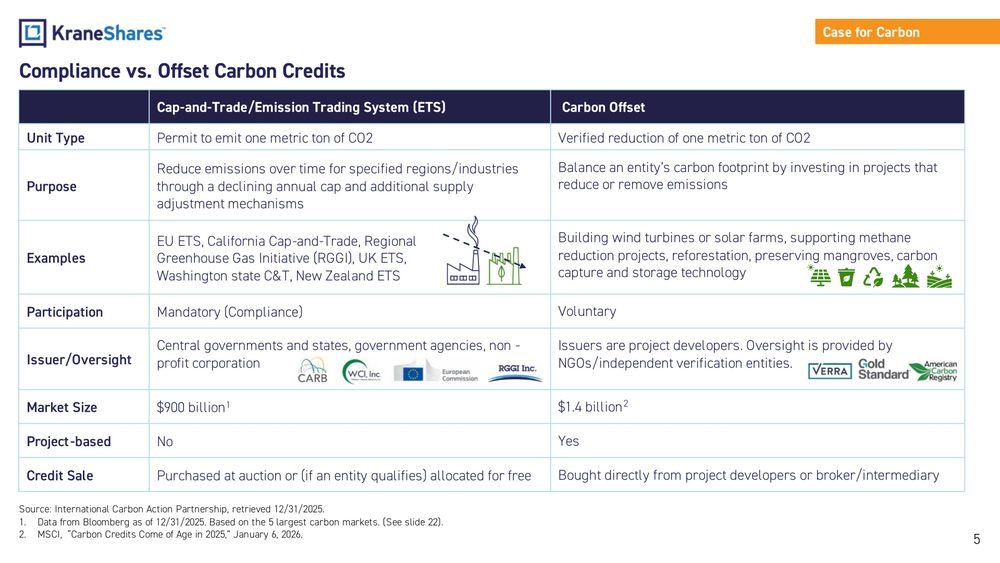

Compliance vs. Offset Carbon Credits

| Cap-and-Trade/Emission Trading System (ETS) | Carbon Offset | |

|---|---|---|

| Unit Type | Permit to emit one metric ton of CO2 | Verified reduction of one metric ton of CO2 |

| Purpose | Reduce emissions over time for specified regions/industries through a declining annual cap and additional supply adjustment mechanisms | Balance an entity's carbon footprint by investing in projects that reduce or remove emissions |

| Examples | EU ETS, California Cap-and-Trade, Regional Greenhouse Gas Initiative (RGGI), UK ETS, Washington state C&T, New Zealand ETS | Building wind turbines or solar farms, supporting methane reduction projects, reforestation, preserving mangroves, carbon capture and storage technology |

| Participation | Mandatory (Compliance) | Voluntary |

| Issuer/Oversight | Central governments and states, government agencies, nonprofit corporation | Issuers are project developers. Oversight is provided by NGOs/independent verification entities. |

| Market Size | $900 billion | $1.4 billion |

| Project-based | No | Yes |

| Credit Sale | Purchased at auction or (if an entity qualifies) allocated for free | Bought directly from project developers or broker/intermediary |

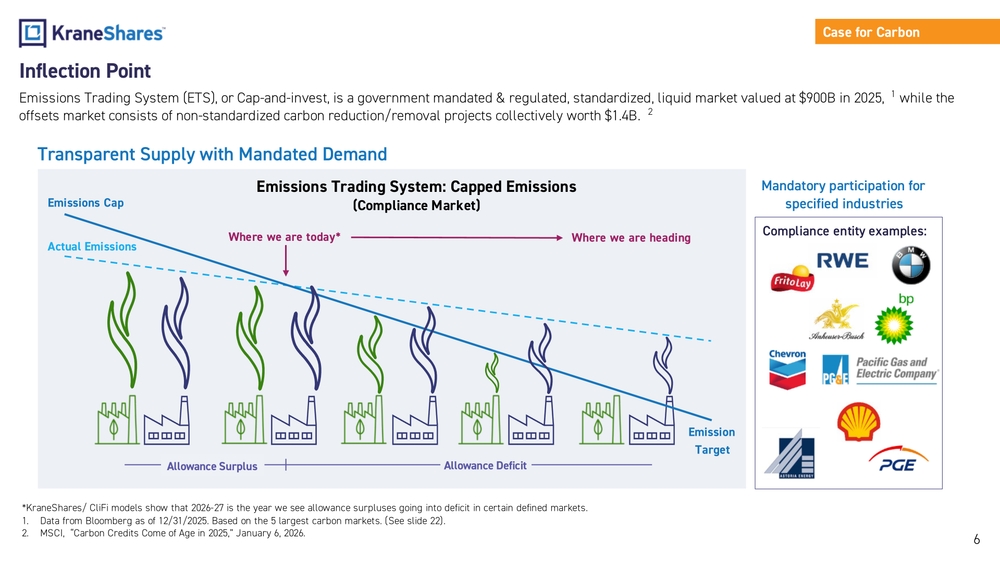

Inflection Point

Emissions Trading System (ETS), or Cap-and-invest, is a government mandated & regulated, standardized, liquid market valued at $900B in 2025, while the offsets market consists of non-standardized carbon reduction/removal projects collectively worth $1.4B.

Transparent Supply with Mandated Demand

Emissions Trading System: Capped Emissions (Compliance Market)

- Emissions Cap declining over time

- Actual Emissions trending below cap

- Transition from Allowance Surplus → Allowance Deficit

- "Where we are today" moving toward "Where we are heading"

- Emission Target drives mandatory compliance

Mandatory participation for specified industries

KraneShares/CliFi models show that 2026-27 is the year we see allowance surpluses going into deficit in certain defined markets.

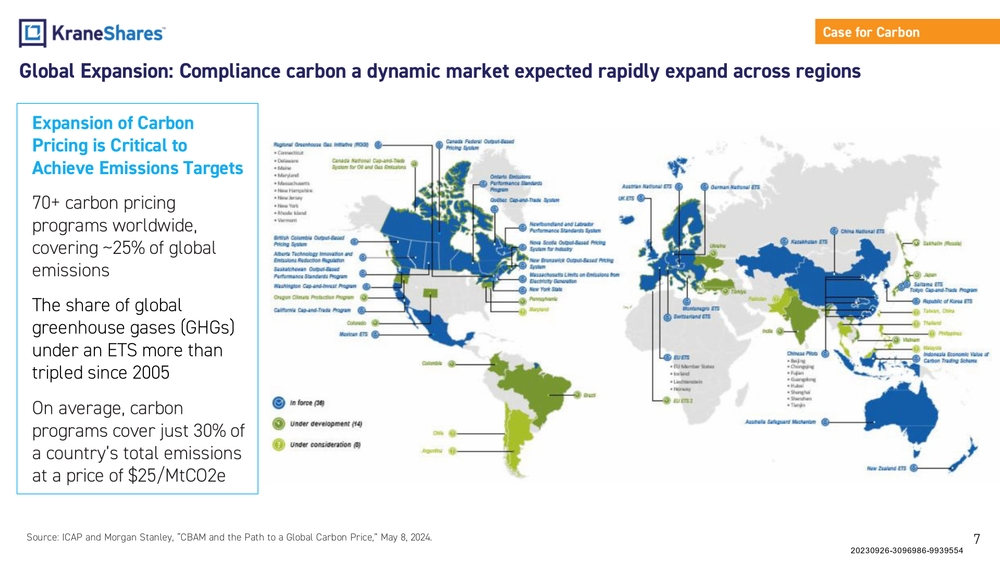

Global Expansion: Compliance carbon a dynamic market expected to rapidly expand across regions

Expansion of Carbon Pricing is Critical to Achieve Emissions Targets

- 70+ carbon pricing programs worldwide, covering ~25% of global emissions

- The share of global greenhouse gases (GHGs) under an ETS more than tripled since 2005

- On average, carbon programs cover just 30% of a country's total emissions at a price of $25/MtCO2e

Programs shown on global map include: In force (38), Under development (14), Under consideration (8)

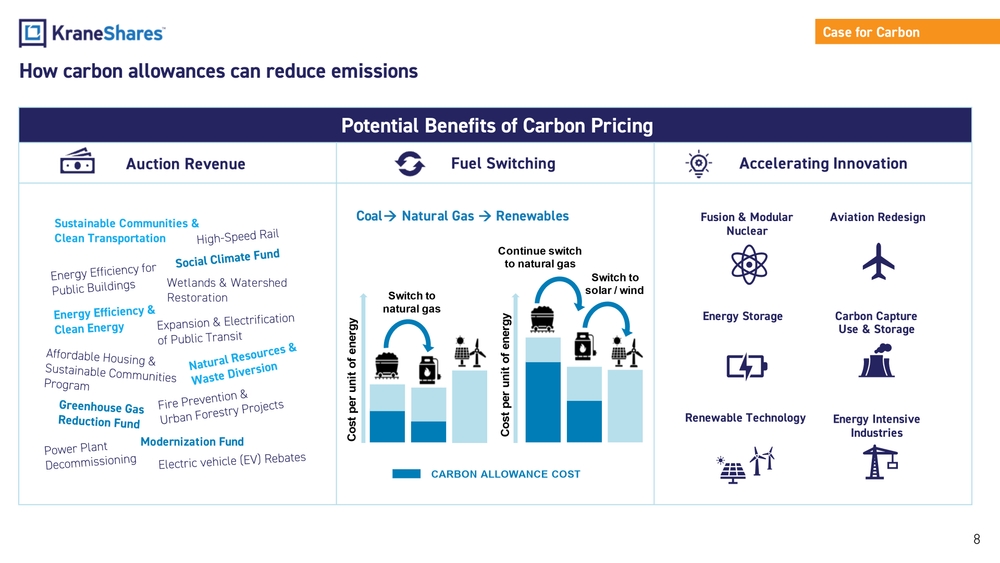

How carbon allowances can reduce emissions

Potential Benefits of Carbon Pricing

Auction Revenue

- Sustainable Communities & Clean Transportation

- High-Speed Rail

- Social Climate Fund

- Energy Efficiency for Public Buildings

- Wetlands & Watershed Restoration

- Energy Efficiency & Clean Energy

- Expansion & Electrification of Public Transit

- Affordable Housing & Sustainable Communities Program

- Natural Resources & Waste Diversion

- Greenhouse Gas Reduction Fund

- Fire Prevention & Urban Forestry Projects

- Power Plant Decommissioning

- Modernization Fund

- Electric vehicle (EV) Rebates

Fuel Switching

- Coal → Natural Gas → Renewables

- Carbon allowance cost drives switching from coal to natural gas, then to solar/wind

Accelerating Innovation

- Fusion & Modular Nuclear

- Aviation Redesign

- Energy Storage

- Carbon Capture Use & Storage

- Renewable Technology

- Energy Intensive Industries

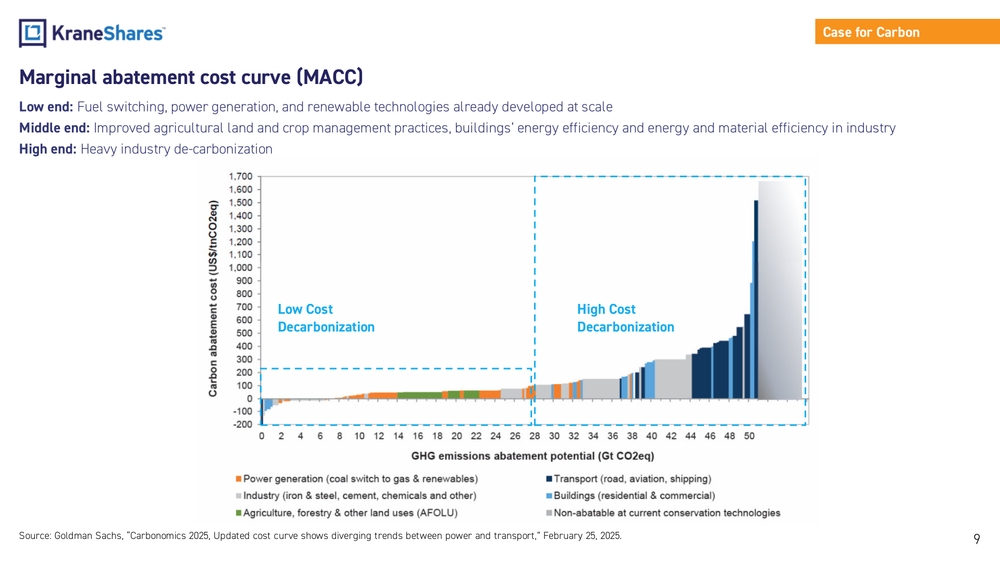

Marginal Abatement Cost Curve (MACC)

Low end: Fuel switching, power generation, and renewable technologies already developed at scale

Middle end: Improved agricultural land and crop management practices, buildings' energy efficiency and energy and material efficiency in industry

High end: Heavy industry de-carbonization

Chart: Carbon abatement cost (US$/tnCO2eq) vs. GHG emissions abatement potential (Gt CO2eq)

- Low Cost Decarbonization (0–26 Gt CO2eq): Power generation, agriculture/forestry, industry

- High Cost Decarbonization (28–50 Gt CO2eq): Transport, buildings, non-abatable sectors

Categories shown:

- Power generation (coal switch to gas & renewables)

- Industry (iron & steel, cement, chemicals and other)

- Agriculture, forestry & other land uses (AFOLU)

- Transport (road, aviation, shipping)

- Buildings (residential & commercial)

- Non-abatable at current conservation technologies

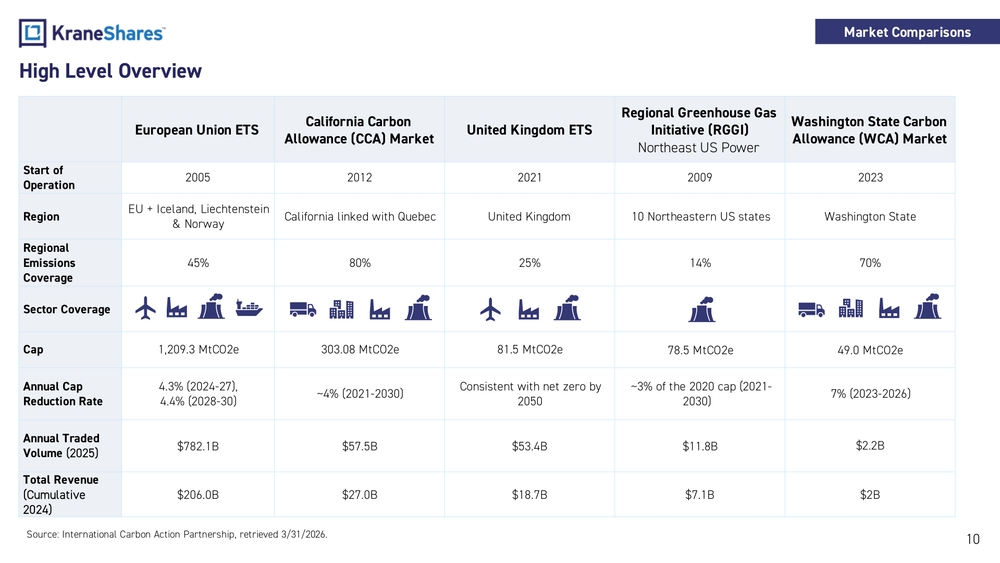

High Level Overview

| European Union ETS | California Carbon Allowance (CCA) Market | United Kingdom ETS | Regional Greenhouse Gas Initiative (RGGI) — Northeast US Power | Washington State Carbon Allowance (WCA) Market | |

|---|---|---|---|---|---|

| Start of Operation | 2005 | 2012 | 2021 | 2009 | 2023 |

| Region | EU + Iceland, Liechtenstein & Norway | California linked with Quebec | United Kingdom | 10 Northeastern US states | Washington State |

| Regional Emissions Coverage | 45% | 80% | 25% | 14% | 70% |

| Cap | 1,209.3 MtCO2e | 303.08 MtCO2e | 81.5 MtCO2e | 78.5 MtCO2e | 49.0 MtCO2e |

| Annual Cap Reduction Rate | 4.3% (2024-27), 4.4% (2028-30) | ~4% (2021-2030) | Consistent with net zero by 2050 | ~3% of the 2020 cap (2021-2030) | 7% (2023-2026) |

| Annual Traded Volume (2025) | $782.1B | $57.5B | $53.4B | $11.8B | $2.2B |

| Total Revenue (Cumulative 2024) | $206.0B | $27.0B | $18.7B | $7.1B | $2B |

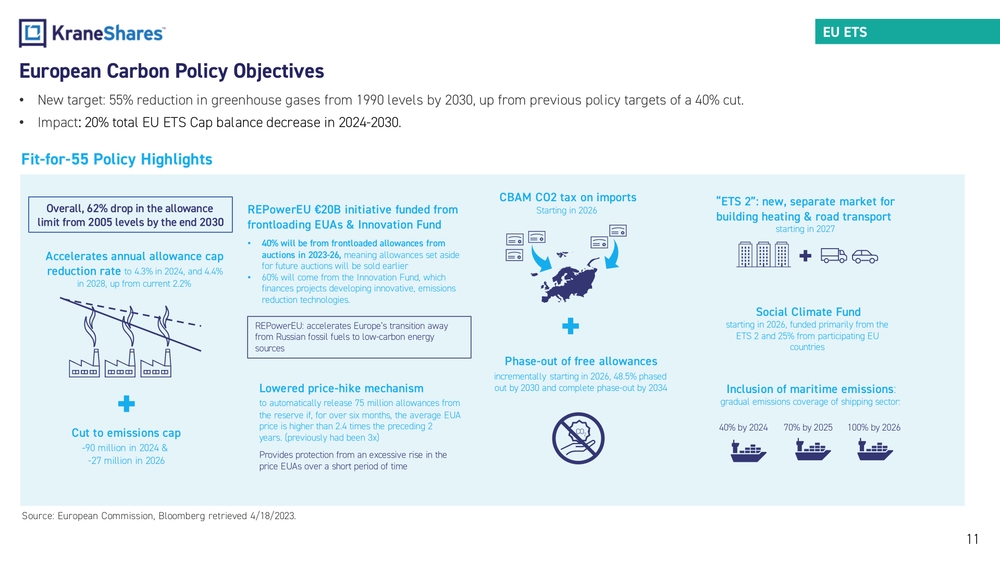

European Carbon Policy Objectives

- New target: 55% reduction in greenhouse gases from 1990 levels by 2030, up from previous policy targets of a 40% cut.

- Impact: 20% total EU ETS Cap balance decrease in 2024-2030.

Fit-for-55 Policy Highlights

Overall, 62% drop in the allowance limit from 2005 levels by the end 2030

Accelerates annual allowance cap reduction rate to 4.3% in 2024, and 4.4% in 2028, up from current 2.2%

Cut to emissions cap: -90 million in 2024 & -27 million in 2026

REPowerEU €20B initiative funded from frontloading EUAs & Innovation Fund

- 40% will be from frontloaded allowances from auctions in 2023-26, meaning allowances set aside for future auctions will be sold earlier

- 60% will come from the Innovation Fund, which finances projects developing innovative, emissions reduction technologies.

- REPowerEU: accelerates Europe's transition away from Russian fossil fuels to low-carbon energy sources

Lowered price-hike mechanism to automatically release 75 million allowances from the reserve if, for over six months, the average EUA price is higher than 2.4 times the preceding 2 years. (previously had been 3x). Provides protection from an excessive rise in the price EUAs over a short period of time.

CBAM CO2 tax on imports Starting in 2026

Phase-out of free allowances incrementally starting in 2026, 48.5% phased out by 2030 and complete phase-out by 2034

"ETS 2": new, separate market for building heating & road transport starting in 2027

Social Climate Fund starting in 2026, funded primarily from the ETS 2 and 25% from participating EU countries

Inclusion of maritime emissions: gradual emissions coverage of shipping sector: 40% by 2024, 70% by 2025, 100% by 2026

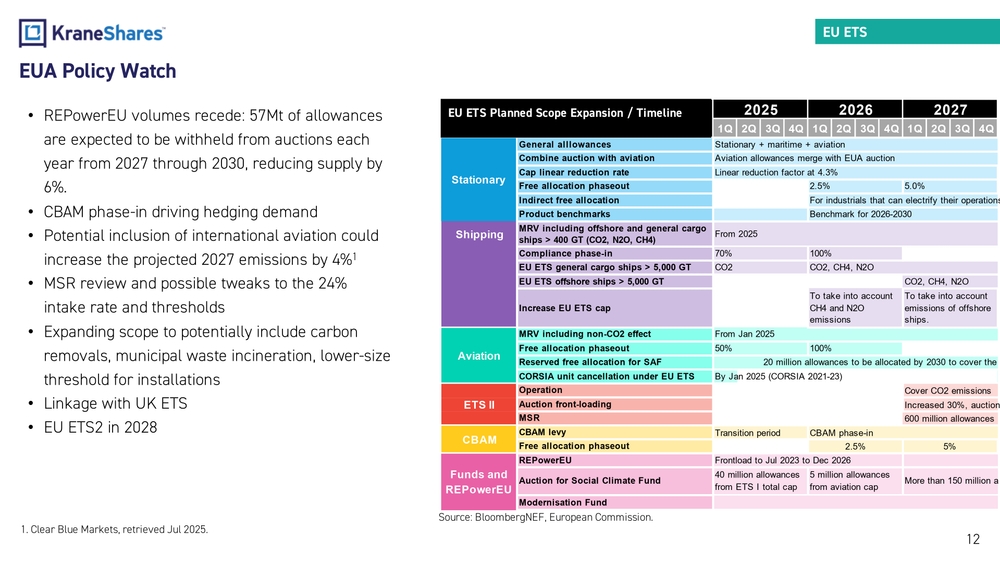

EUA Policy Watch

- REPowerEU volumes recede: 57Mt of allowances are expected to be withheld from auctions each year from 2027 through 2030, reducing supply by 6%.

- CBAM phase-in driving hedging demand

- Potential inclusion of international aviation could increase the projected 2027 emissions by 4%

- MSR review and possible tweaks to the 24% intake rate and thresholds

- Expanding scope to potentially include carbon removals, municipal waste incineration, lower-size threshold for installations

- Linkage with UK ETS

- EU ETS2 in 2028

EU ETS Planned Scope Expansion / Timeline

Stationary

- General allowances: Stationary + maritime + aviation

- Combine auction with aviation: Aviation allowances merge with EUA auction

- Cap linear reduction rate: Linear reduction factor at 4.3%

- Free allocation phaseout: 2.5% (2026), 5.0% (2027)

- Indirect free allocation: For industrials that can electrify their operations

- Product benchmarks: Benchmark for 2026-2030

Shipping

- MRV including offshore and general cargo ships > 400 GT (CO2, N2O, CH4): From 2025

- Compliance phase-in: 70% (2025), 100% (2026)

- EU ETS general cargo ships > 5,000 GT: CO2 (2025), CO2, CH4, N2O (2026)

- EU ETS offshore ships > 5,000 GT: CO2, CH4, N2O (2027)

- Increase EU ETS cap: To take into account CH4 and N2O emissions (2026); To take into account emissions of offshore ships (2027)

Aviation

- MRV including non-CO2 effect: From Jan 2025

- Free allocation phaseout: 50% (2025), 100% (2026)

- Reserved free allocation for SAF: 20 million allowances to be allocated by 2030

- CORSIA unit cancellation under EU ETS: By Jan 2025 (CORSIA 2021-23)

ETS II

- Operation: Cover CO2 emissions (2027)

- Auction front-loading: Increased 30% (2027)

- MSR: 600 million allowances (2027)

CBAM

- CBAM levy: Transition period (2025), CBAM phase-in (2026)

- Free allocation phaseout: 2.5% (2026), 5% (2027)

Funds and REPowerEU

- REPowerEU: Frontload to Jul 2023 to Dec 2026

- Auction for Social Climate Fund: 40 million allowances from ETS I total cap (2025); 5 million allowances from aviation cap (2026); More than 150 million (2027)

- Modernisation Fund

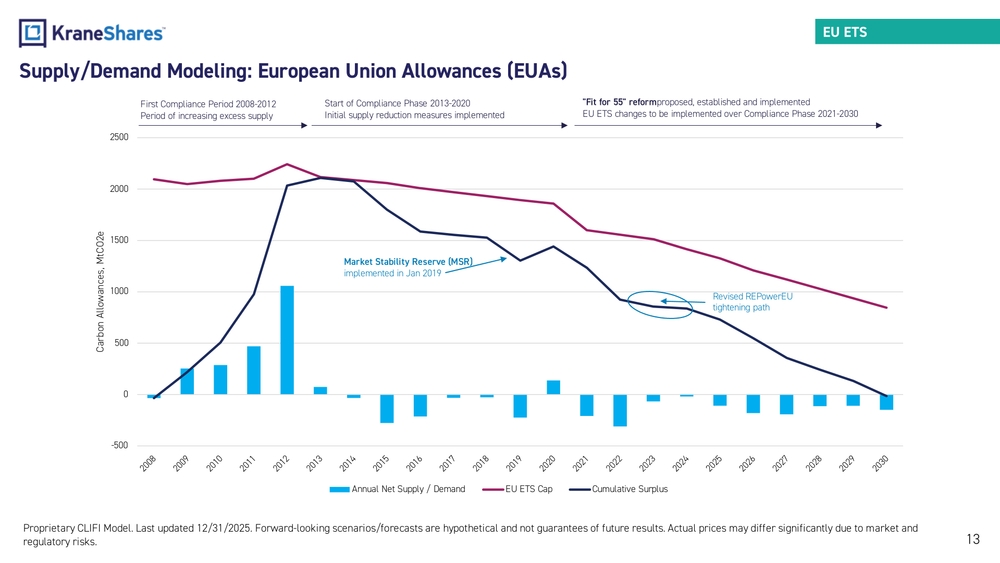

Supply/Demand Modeling: European Union Allowances (EUAs)

Key Phases

- First Compliance Period 2008-2012: Period of increasing excess supply

- Start of Compliance Phase 2013-2020: Initial supply reduction measures implemented

- "Fit for 55" reform proposed, established and implemented; EU ETS changes to be implemented over Compliance Phase 2021-2030

- Market Stability Reserve (MSR) implemented in Jan 2019

- Revised REPowerEU tightening path

Chart shows Annual Net Supply / Demand, EU ETS Cap, and Cumulative Surplus from 2008 to 2030.

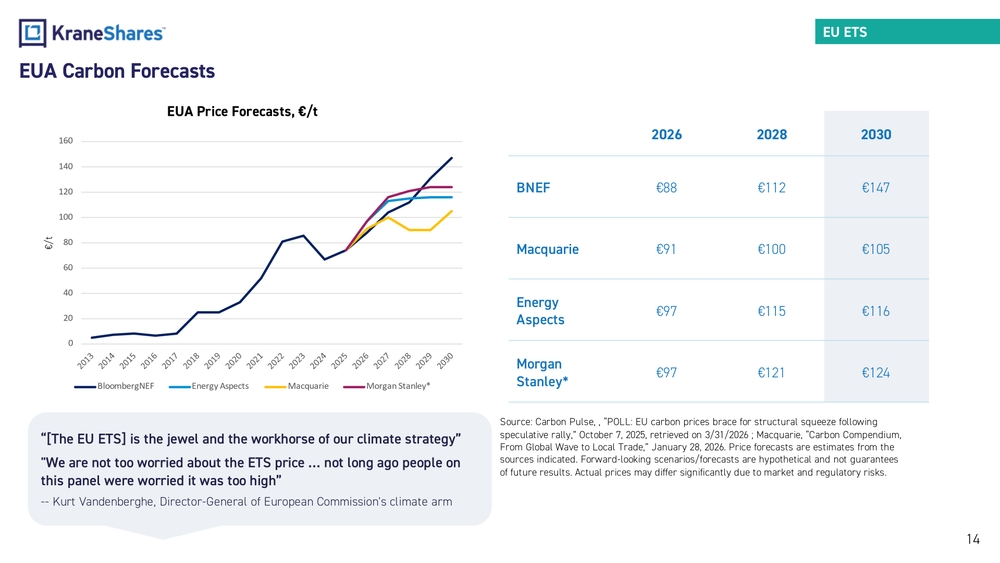

EUA Carbon Forecasts

EUA Price Forecasts, €/t

| 2026 | 2028 | 2030 | |

|---|---|---|---|

| BNEF | €88 | €112 | €147 |

| Macquarie | €91 | €100 | €105 |

| Energy Aspects | €97 | €115 | €116 |

| Morgan Stanley* | €97 | €121 | €124 |

"[The EU ETS] is the jewel and the workhorse of our climate strategy"

"We are not too worried about the ETS price … not long ago people on this panel were worried it was too high"

-- Kurt Vandenberghe, Director-General of European Commission's climate arm

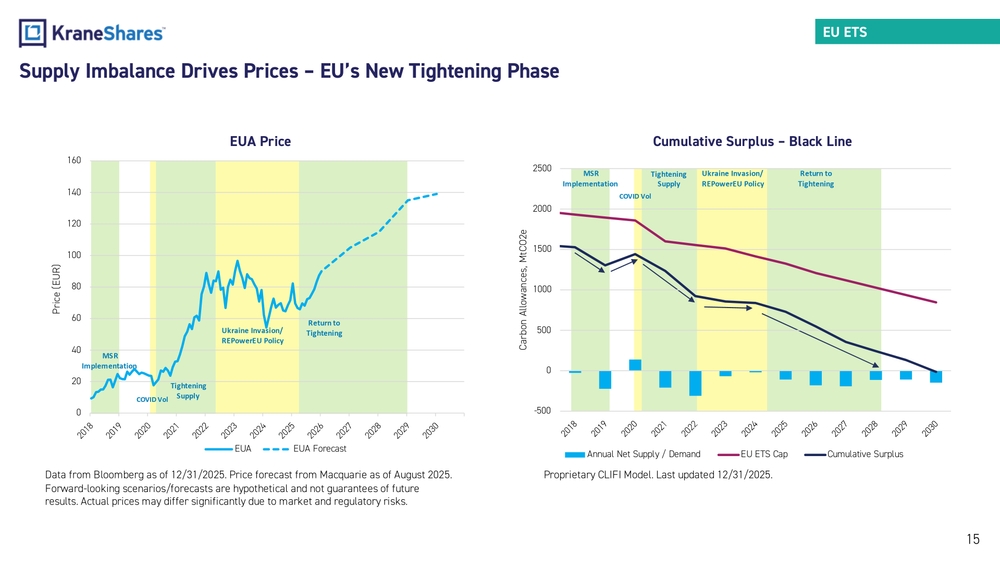

Supply Imbalance Drives Prices – EU's New Tightening Phase

EUA Price

Chart shows EUA price history and forecast (EUR) from 2018 to 2030, with key phases annotated:

- MSR Implementation

- COVID Vol

- Tightening Supply

- Ukraine Invasion / REPowerEU Policy

- Return to Tightening

Cumulative Surplus – Black Line

Chart shows Annual Net Supply / Demand, EU ETS Cap, and Cumulative Surplus (MtCO2e) from 2018 to 2030, with the same key phases annotated.

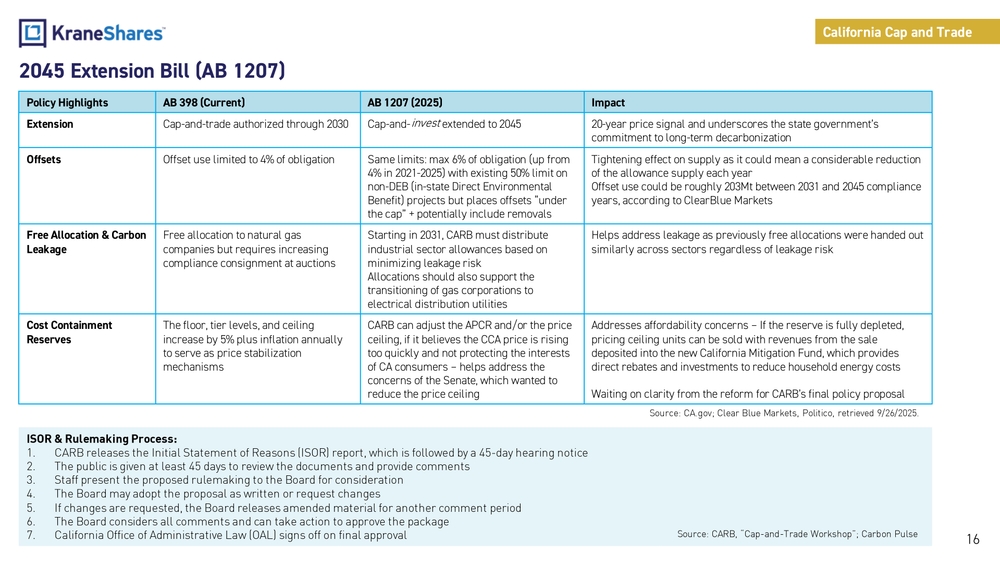

2045 Extension Bill (AB 1207)

California Cap and Trade

| Policy Highlights | AB 398 (Current) | AB 1207 (2025) | Impact |

|---|---|---|---|

| Extension | Cap-and-trade authorized through 2030 | Cap-and-invest extended to 2045 | 20-year price signal and underscores the state government's commitment to long-term decarbonization |

| Offsets | Offset use limited to 4% of obligation | Same limits: max 6% of obligation (up from 4% in 2021-2025) with existing 50% limit on non-DEB (in-state Direct Environmental Benefit) projects but places offsets "under the cap" + potentially include removals | Tightening effect on supply as it could mean a considerable reduction of the allowance supply each year. Offset use could be roughly 203Mt between 2031 and 2045 compliance years, according to ClearBlue Markets |

| Free Allocation & Carbon Leakage | Free allocation to natural gas companies but requires increasing compliance consignment at auctions | Starting in 2031, CARB must distribute industrial sector allowances based on minimizing leakage risk. Allocations should also support the transitioning of gas corporations to electrical distribution utilities | Helps address leakage as previously free allocations were handed out similarly across sectors regardless of leakage risk |

| Cost Containment Reserves | The floor, tier levels, and ceiling increase by 5% plus inflation annually to serve as price stabilization mechanisms | CARB can adjust the APCR and/or the price ceiling, if it believes the CCA price is rising too quickly and not protecting the interests of CA consumers – helps address the concerns of the Senate, which wanted to reduce the price ceiling | Addresses affordability concerns – If the reserve is fully depleted, pricing ceiling units can be sold with revenues from the sale deposited into the new California Mitigation Fund, which provides direct rebates and investments to reduce household energy costs. Waiting on clarity from the reform for CARB's final policy proposal |

ISOR & Rulemaking Process:

- CARB releases the Initial Statement of Reasons (ISOR) report, which is followed by a 45-day hearing notice

- The public is given at least 45 days to review the documents and provide comments

- Staff present the proposed rulemaking to the Board for consideration

- The Board may adopt the proposal as written or request changes

- If changes are requested, the Board releases amended material for another comment period

- The Board considers all comments and can take action to approve the package

- California Office of Administrative Law (OAL) signs off on final approval

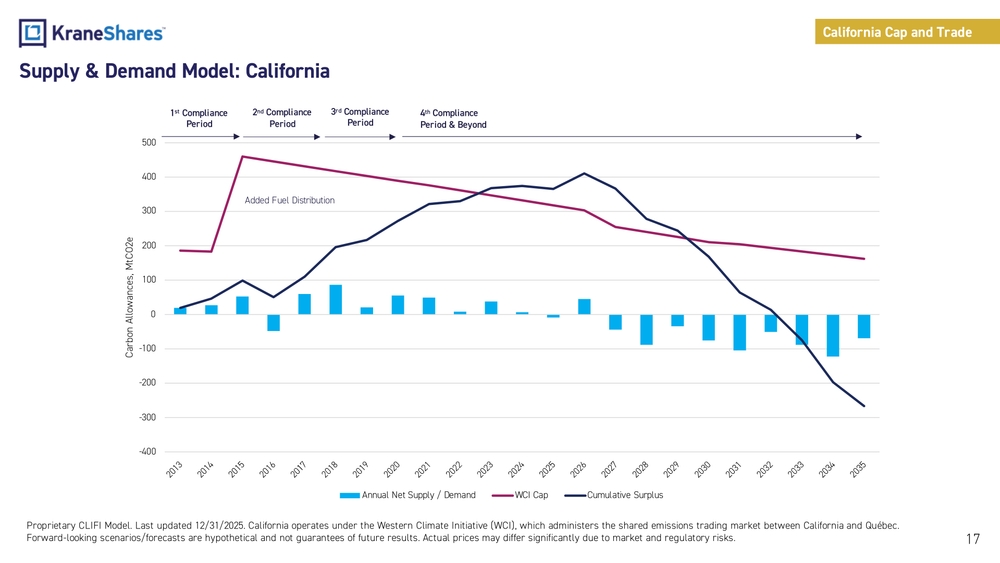

Supply & Demand Model: California

California Cap and Trade

Chart shows Annual Net Supply / Demand, WCI Cap, and Cumulative Surplus (MtCO2e) from 2013 to 2035, across four compliance periods:

- 1st Compliance Period

- 2nd Compliance Period

- 3rd Compliance Period

- 4th Compliance Period & Beyond

- Added Fuel Distribution (noted during 2nd compliance period)

California operates under the Western Climate Initiative (WCI), which administers the shared emissions trading market between California and Québec.

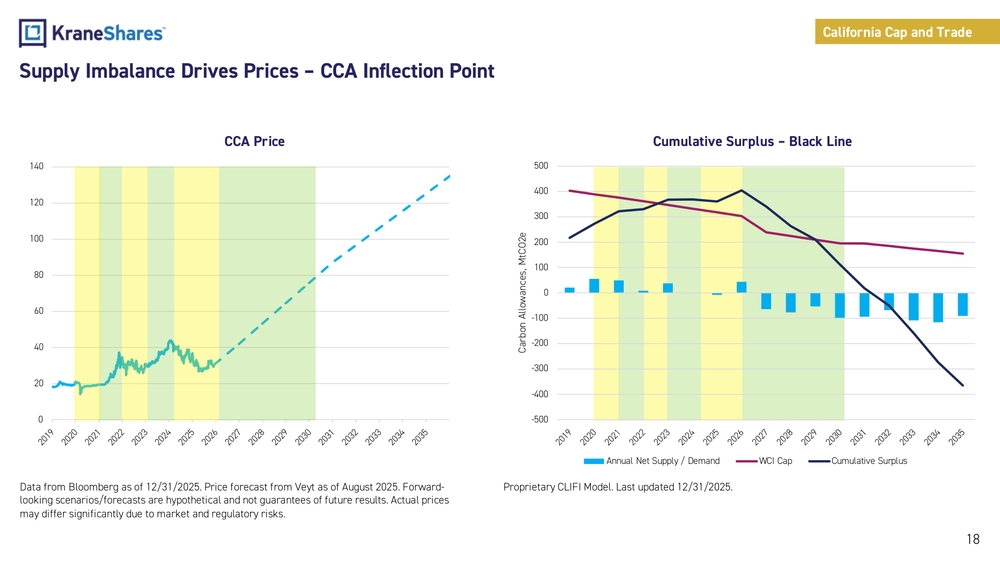

Supply Imbalance Drives Prices – CCA Inflection Point

California Cap and Trade

CCA Price

Chart shows CCA price history and forecast from 2019 to 2035, with price rising from ~$20 to a projected ~$130+ by 2035.

Cumulative Surplus – Black Line

Chart shows Annual Net Supply / Demand, WCI Cap, and Cumulative Surplus (MtCO2e) from 2019 to 2035. The cumulative surplus peaks around 2026 and then declines sharply into deficit territory.

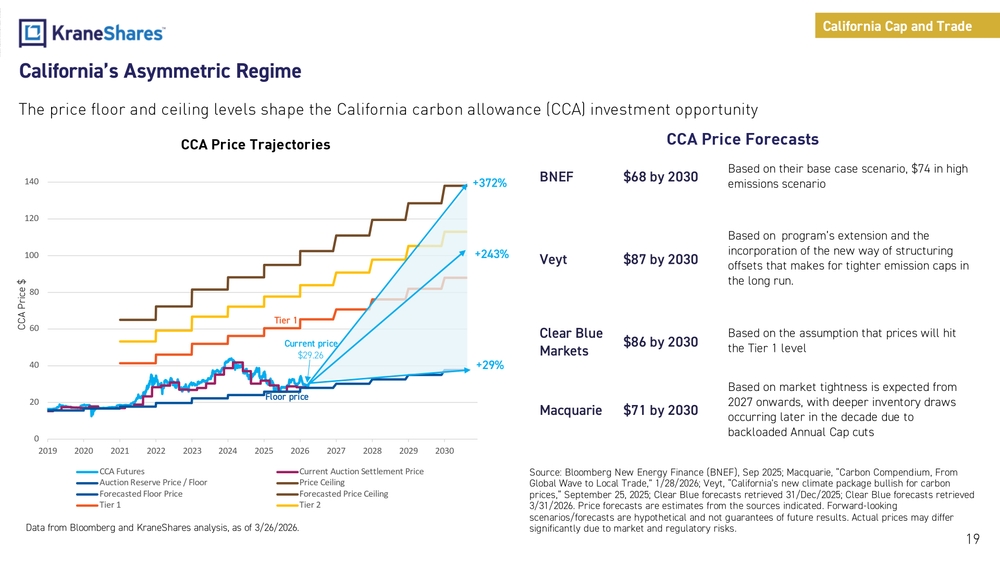

California's Asymmetric Regime

The price floor and ceiling levels shape the California carbon allowance (CCA) investment opportunity

CCA Price Trajectories

Chart shows CCA price trajectories from 2019 to 2030, including CCA Futures, Current Auction Settlement Price, Auction Reserve Price / Floor, Price Ceiling, Forecasted Floor Price, Forecasted Price Ceiling, Tier 1, and Tier 2.

- Current price: $29.26

- Floor price trajectory shown

- +372% (Price Ceiling trajectory)

- +243% (Tier 2 trajectory)

- +29% (Floor price trajectory)

CCA Price Forecasts

| Forecaster | Forecast | Rationale |

|---|---|---|

| BNEF | $68 by 2030 | Based on their base case scenario, $74 in high emissions scenario |

| Veyt | $87 by 2030 | Based on program's extension and the incorporation of the new way of structuring offsets that makes for tighter emission caps in the long run |

| Clear Blue Markets | $86 by 2030 | Based on the assumption that prices will hit the Tier 1 level |

| Macquarie | $71 by 2030 | Based on market tightness expected from 2027 onwards, with deeper inventory draws occurring later in the decade due to backloaded Annual Cap cuts |

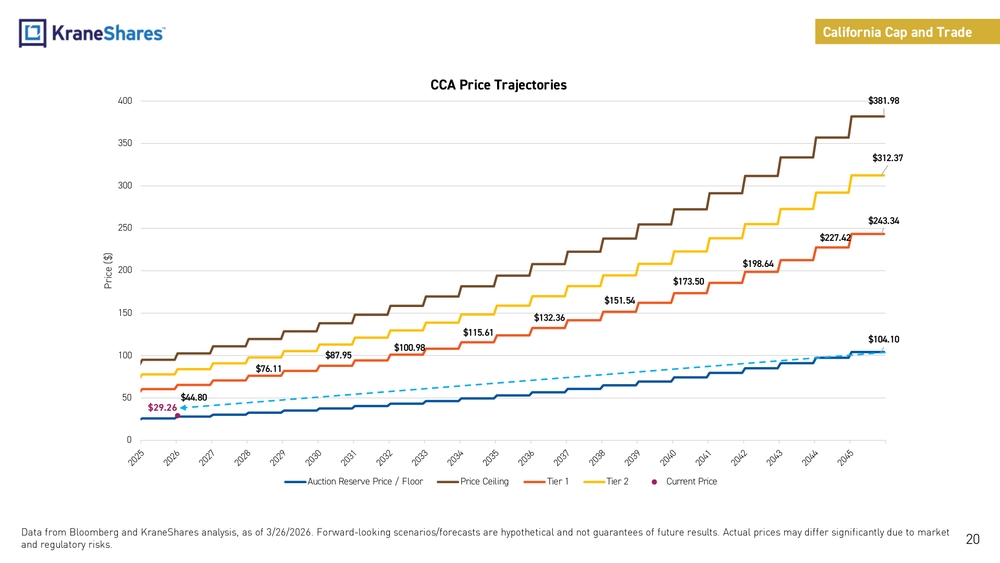

CCA Price Trajectories

California Cap and Trade

Chart shows CCA price trajectories from 2025 to 2045, including:

- Auction Reserve Price / Floor

- Price Ceiling

- Tier 1

- Tier 2

- Current Price

Key Price Points (2045 projections):

- Price Ceiling: $381.98

- Tier 2: $312.37

- Tier 1: $243.34

- Tier 2 (lower): $227.42

- Tier 1 (lower): $198.64

- $173.50

- $151.54

- $132.36

- $115.61

- $100.98

- $87.95

- $76.11

- Auction Reserve Price / Floor: $104.10

- Current Price: $29.26

- $44.80 (near-term reference point)

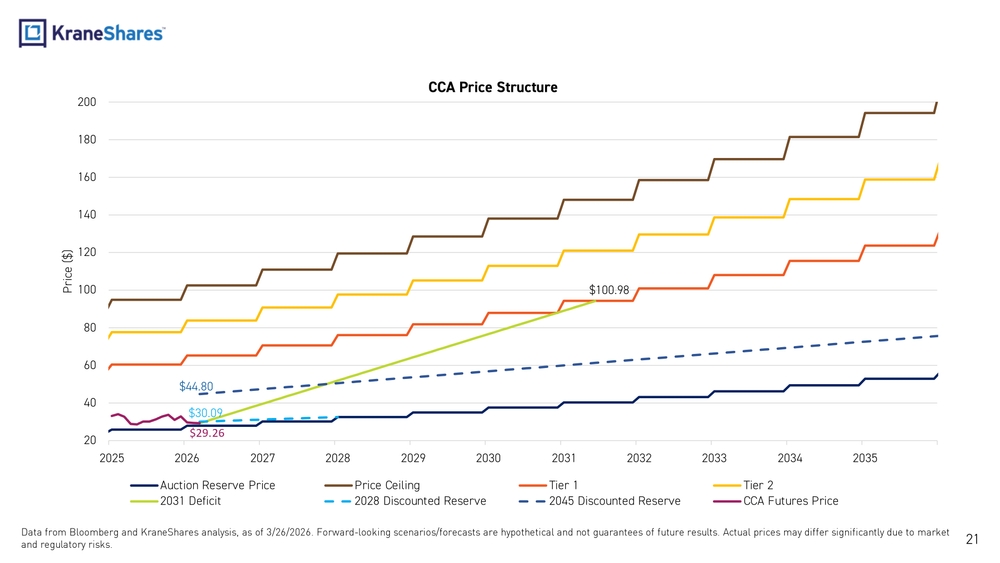

CCA Price Structure

Price Data Points

- $100.98 (2031 Deficit projection)

- $44.80 (2028 Discounted Reserve)

- $30.09 (2045 Discounted Reserve)

- $29.26 (CCA Futures Price)

Legend

- Auction Reserve Price

- Price Ceiling

- Tier 1

- Tier 2

- 2031 Deficit

- 2028 Discounted Reserve

- 2045 Discounted Reserve

- CCA Futures Price

Chart covers price projections from 2025 to 2035.

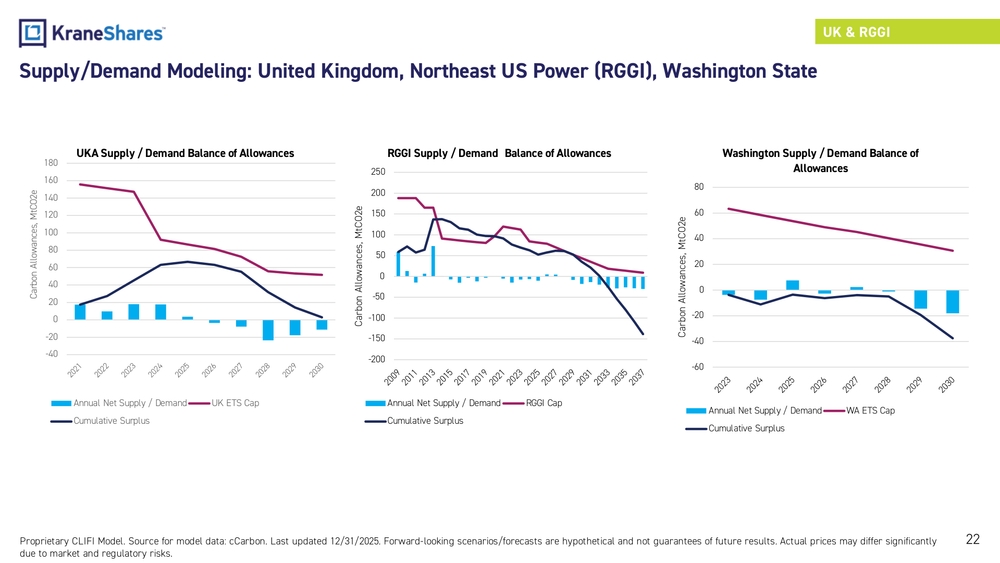

Supply/Demand Modeling: United Kingdom, Northeast US Power (RGGI), Washington State

UKA Supply / Demand Balance of Allowances

- Annual Net Supply / Demand vs. UK ETS Cap

- Cumulative Surplus trend shown from 2021–2030

RGGI Supply / Demand Balance of Allowances

- Annual Net Supply / Demand vs. RGGI Cap

- Cumulative Surplus trend shown from 2009–2037

Washington Supply / Demand Balance of Allowances

- Annual Net Supply / Demand vs. WA ETS Cap

- Cumulative Surplus trend shown from 2023–2030

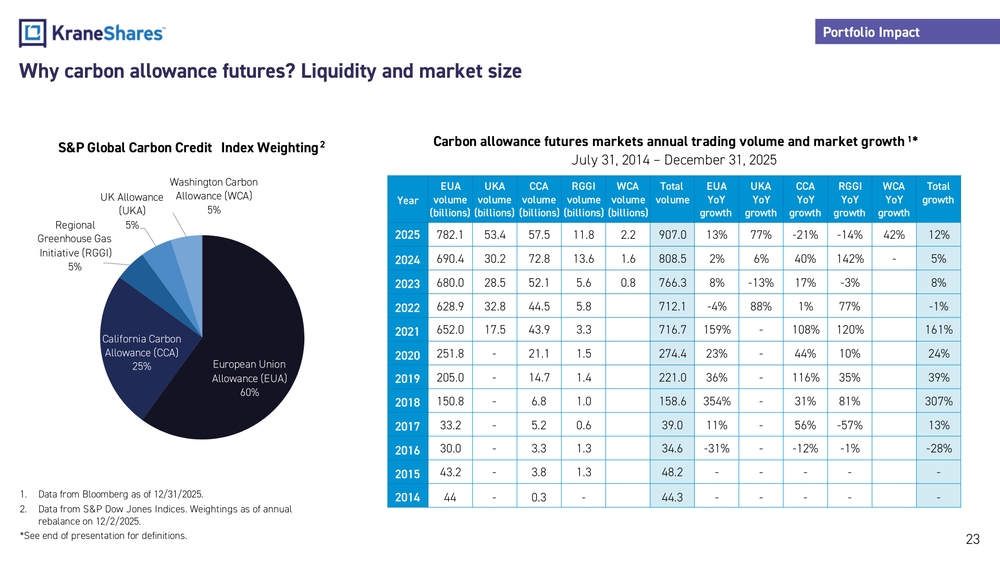

Why carbon allowance futures? Liquidity and market size

Carbon allowance futures markets annual trading volume and market growth

July 31, 2014 – December 31, 2025

| Year | EUA volume (billions) | UKA volume (billions) | CCA volume (billions) | RGGI volume (billions) | WCA volume (billions) | Total volume | EUA YoY growth | UKA YoY growth | CCA YoY growth | RGGI YoY growth | WCA YoY growth | Total growth |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2025 | 782.1 | 53.4 | 57.5 | 11.8 | 2.2 | 907.0 | 13% | 77% | -21% | -14% | 42% | 12% |

| 2024 | 690.4 | 30.2 | 72.8 | 13.6 | 1.6 | 808.5 | 2% | 6% | 40% | 142% | - | 5% |

| 2023 | 680.0 | 28.5 | 52.1 | 5.6 | 0.8 | 766.3 | 8% | -13% | 17% | -3% | - | 8% |

| 2022 | 628.9 | 32.8 | 44.5 | 5.8 | - | 712.1 | -4% | 88% | 1% | 77% | - | -1% |

| 2021 | 652.0 | 17.5 | 43.9 | 3.3 | - | 716.7 | 159% | - | 108% | 120% | - | 161% |

| 2020 | 251.8 | - | 21.1 | 1.5 | - | 274.4 | 23% | - | 44% | 10% | - | 24% |

| 2019 | 205.0 | - | 14.7 | 1.4 | - | 221.0 | 36% | - | 116% | 35% | - | 39% |

| 2018 | 150.8 | - | 6.8 | 1.0 | - | 158.6 | 354% | - | 31% | 81% | - | 307% |

| 2017 | 33.2 | - | 5.2 | 0.6 | - | 39.0 | 11% | - | 56% | -57% | - | 13% |

| 2016 | 30.0 | - | 3.3 | 1.3 | - | 34.6 | -31% | - | -12% | -1% | - | -28% |

| 2015 | 43.2 | - | 3.8 | 1.3 | - | 48.2 | - | - | - | - | - | - |

| 2014 | 44 | - | 0.3 | - | - | 44.3 | - | - | - | - | - | - |

S&P Global Carbon Credit Index Weighting

- European Union Allowance (EUA): 60%

- California Carbon Allowance (CCA): 25%

- Regional Greenhouse Gas Initiative (RGGI): 5%

- UK Allowance (UKA): 5%

- Washington Carbon Allowance (WCA): 5%

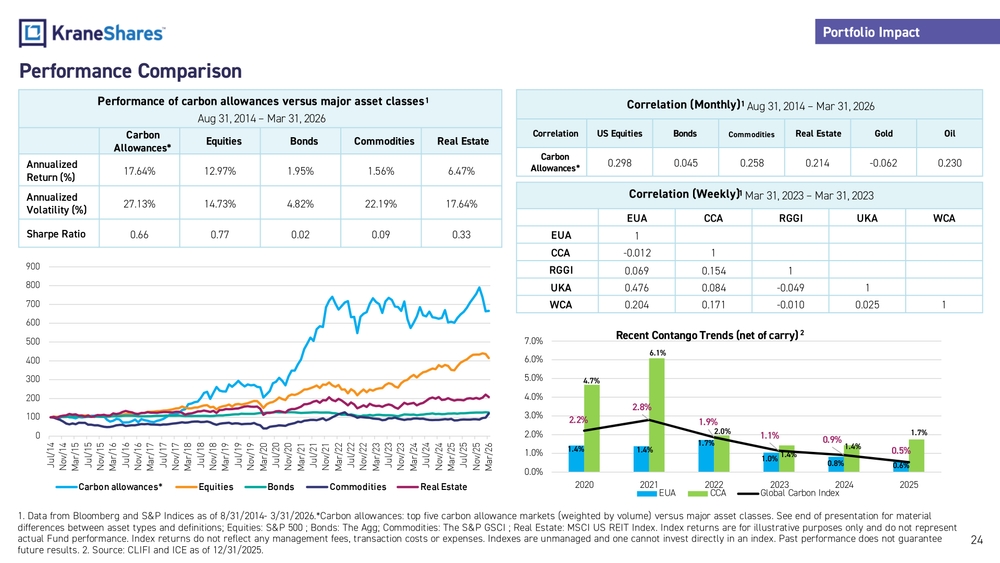

Performance Comparison

Performance of carbon allowances versus major asset classes

Aug 31, 2014 – Mar 31, 2026

| Carbon Allowances* | Equities | Bonds | Commodities | Real Estate | |

|---|---|---|---|---|---|

| Annualized Return (%) | 17.64% | 12.97% | 1.95% | 1.56% | 6.47% |

| Annualized Volatility (%) | 27.13% | 14.73% | 4.82% | 22.19% | 17.64% |

| Sharpe Ratio | 0.66 | 0.77 | 0.02 | 0.09 | 0.33 |

Correlation (Monthly) Aug 31, 2014 – Mar 31, 2026

| Correlation | US Equities | Bonds | Commodities | Real Estate | Gold | Oil |

|---|---|---|---|---|---|---|

| Carbon Allowances* | 0.298 | 0.045 | 0.258 | 0.214 | -0.062 | 0.230 |

Correlation (Weekly) Mar 31, 2023 – Mar 31, 2023

| EUA | CCA | RGGI | UKA | WCA | |

|---|---|---|---|---|---|

| EUA | 1 | ||||

| CCA | -0.012 | 1 | |||

| RGGI | 0.069 | 0.154 | 1 | ||

| UKA | 0.476 | 0.084 | -0.049 | 1 | |

| WCA | 0.204 | 0.171 | -0.010 | 0.025 | 1 |

Recent Contango Trends (net of carry)

- 2020: EUA 2.2%, CCA 1.4%, Global Carbon Index 1.4%

- 2021: EUA 4.7%, CCA 1.4%, Global Carbon Index 1.7%

- 2022: EUA 6.1%, CCA 2.8%, Global Carbon Index 2.0% (approx.)

- 2023: EUA 1.9%, CCA 1.7%, Global Carbon Index 2.0%

- 2024: EUA 1.1%, CCA 1.0%, Global Carbon Index 1.4%

- 2025: EUA 0.9%, CCA 0.8%, Global Carbon Index 1.4%

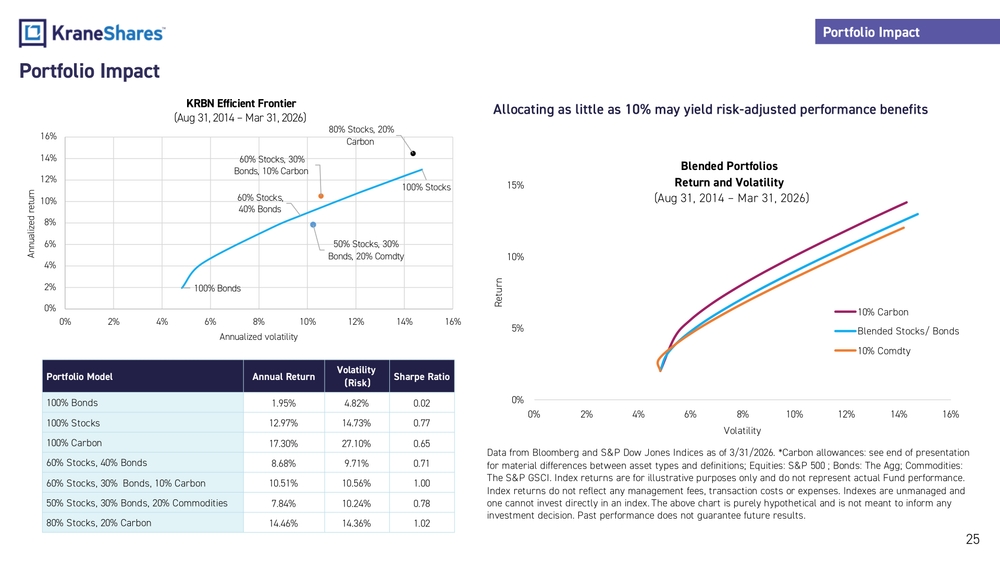

Portfolio Impact

Allocating as little as 10% may yield risk-adjusted performance benefits

Portfolio Model Comparison (Aug 31, 2014 – Mar 31, 2026)

| Portfolio Model | Annual Return | Volatility (Risk) | Sharpe Ratio |

|---|---|---|---|

| 100% Bonds | 1.95% | 4.82% | 0.02 |

| 100% Stocks | 12.97% | 14.73% | 0.77 |

| 100% Carbon | 17.30% | 27.10% | 0.65 |

| 60% Stocks, 40% Bonds | 8.68% | 9.71% | 0.71 |

| 60% Stocks, 30% Bonds, 10% Carbon | 10.51% | 10.56% | 1.00 |

| 50% Stocks, 30% Bonds, 20% Commodities | 7.84% | 10.24% | 0.78 |

| 80% Stocks, 20% Carbon | 14.46% | 14.36% | 1.02 |

KRBN Efficient Frontier

(Aug 31, 2014 – Mar 31, 2026)

Blended Portfolios Return and Volatility chart shows that adding carbon (10% Carbon blend) improves the return/volatility profile compared to blended stocks/bonds or 10% commodities allocations.

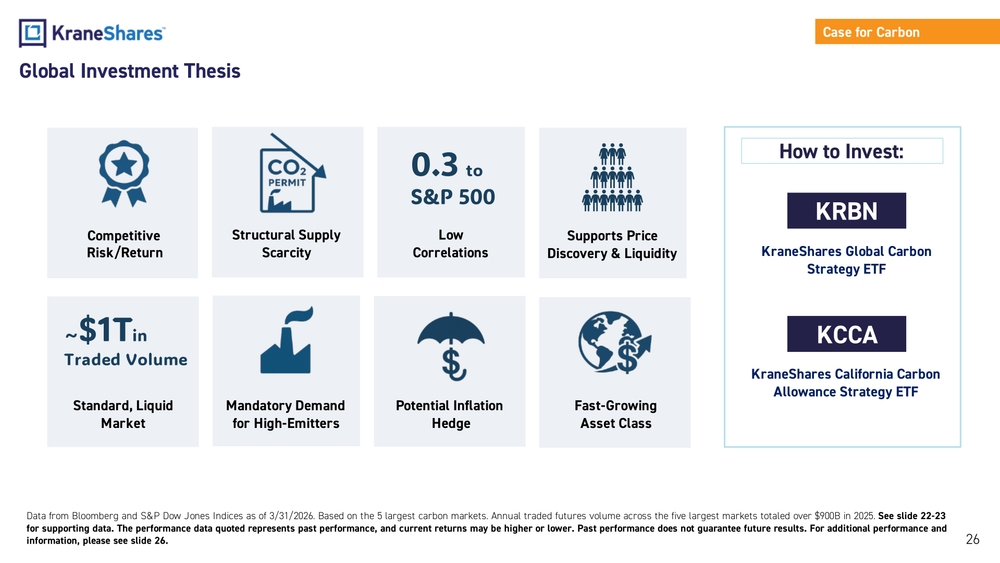

Global Investment Thesis

Case for Carbon

- Competitive Risk/Return

- Structural Supply Scarcity

- Low Correlations — 0.3 to S&P 500

- Supports Price Discovery & Liquidity — Mandatory Demand for High-Emitters

- ~$1T in Traded Volume — Standard, Liquid Market

- Potential Inflation Hedge

- Fast-Growing Asset Class

How to Invest:

KRBN — KraneShares Global Carbon Strategy ETF

KCCA — KraneShares California Carbon Allowance Strategy ETF

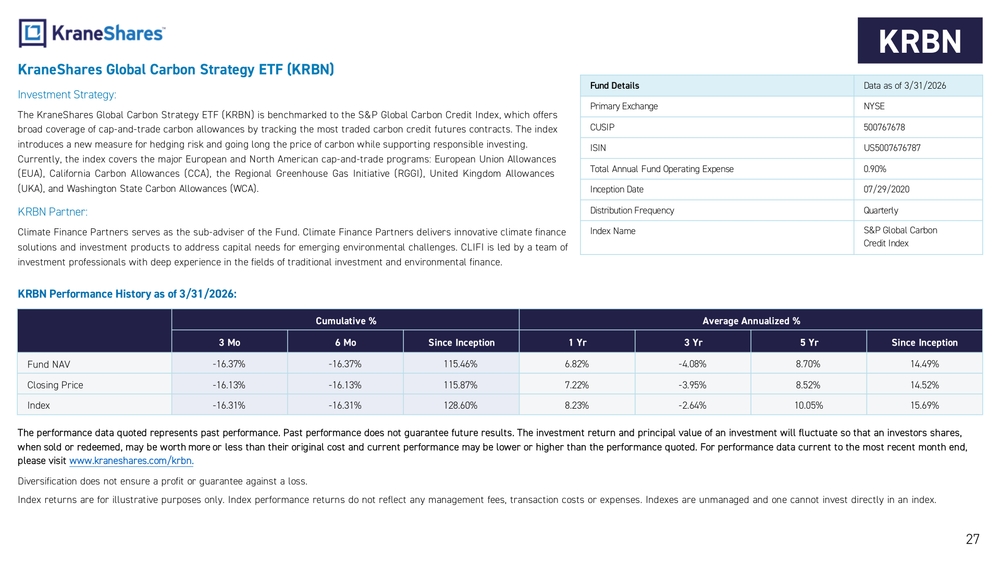

KraneShares Global Carbon Strategy ETF (KRBN)

Investment Strategy

The KraneShares Global Carbon Strategy ETF (KRBN) is benchmarked to the S&P Global Carbon Credit Index, which offers broad coverage of cap-and-trade carbon allowances by tracking the most traded carbon credit futures contracts. The index introduces a new measure for hedging risk and going long the price of carbon while supporting responsible investing. Currently, the index covers the major European and North American cap-and-trade programs: European Union Allowances (EUA), California Carbon Allowances (CCA), the Regional Greenhouse Gas Initiative (RGGI), United Kingdom Allowances (UKA), and Washington State Carbon Allowances (WCA).

KRBN Partner

Climate Finance Partners serves as the sub-adviser of the Fund. Climate Finance Partners delivers innovative climate finance solutions and investment products to address capital needs for emerging environmental challenges. CLIFI is led by a team of investment professionals with deep experience in the fields of traditional investment and environmental finance.

Fund Details (Data as of 3/31/2026)

- Primary Exchange: NYSE

- CUSIP: 500767678

- ISIN: US5007676787

- Total Annual Fund Operating Expense: 0.90%

- Inception Date: 07/29/2020

- Distribution Frequency: Quarterly

- Index Name: S&P Global Carbon Credit Index

KRBN Performance History as of 3/31/2026

| 3 Mo | 6 Mo | Since Inception | 1 Yr | 3 Yr | 5 Yr | Since Inception | |

|---|---|---|---|---|---|---|---|

| Fund NAV | -16.37% | -16.37% | 115.46% | 6.82% | -4.08% | 8.70% | 14.49% |

| Closing Price | -16.13% | -16.13% | 115.87% | 7.22% | -3.95% | 8.52% | 14.52% |

| Index | -16.31% | -16.31% | 128.60% | 8.23% | -2.64% | 10.05% | 15.69% |

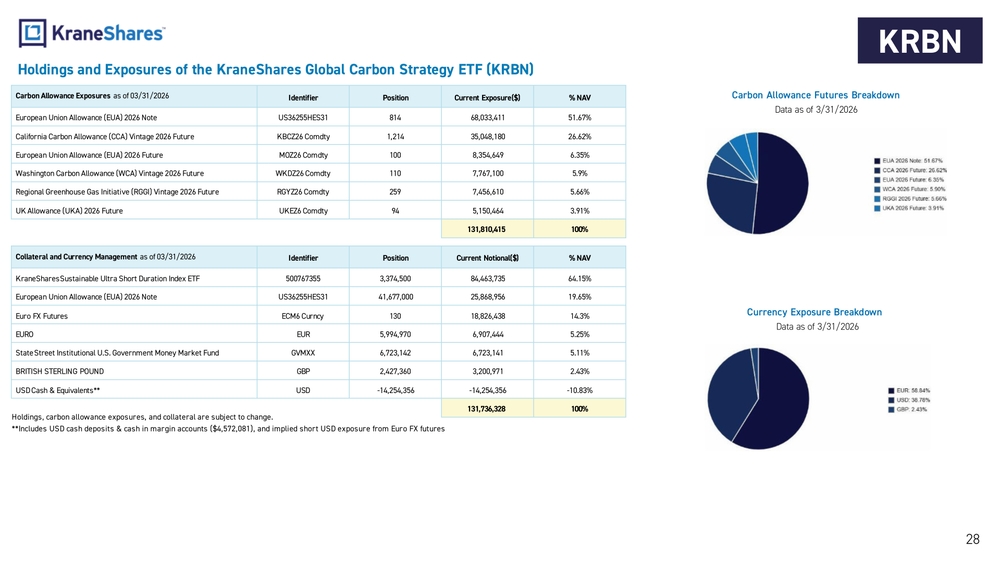

Holdings and Exposures of the KraneShares Global Carbon Strategy ETF (KRBN)

Carbon Allowance Exposures as of 03/31/2026

| Carbon Allowance | Identifier | Position | Current Exposure($) | % NAV |

|---|---|---|---|---|

| European Union Allowance (EUA) 2026 Note | US36255HES31 | 814 | 68,033,411 | 51.67% |

| California Carbon Allowance (CCA) Vintage 2026 Future | KBCZ26 Comdty | 1,214 | 35,048,180 | 26.62% |

| European Union Allowance (EUA) 2026 Future | MOZ26 Comdty | 100 | 8,354,649 | 6.35% |

| Washington Carbon Allowance (WCA) Vintage 2026 Future | WKDZ26 Comdty | 110 | 7,767,100 | 5.9% |

| Regional Greenhouse Gas Initiative (RGGI) Vintage 2026 Future | RGYZ26 Comdty | 259 | 7,456,610 | 5.66% |

| UK Allowance (UKA) 2026 Future | UKEZ6 Comdty | 94 | 5,150,464 | 3.91% |

| Total | 131,810,415 | 100% |

Collateral and Currency Management as of 03/31/2026

| Holding | Identifier | Position | Current Notional($) | % NAV |

|---|---|---|---|---|

| KraneShares Sustainable Ultra Short Duration Index ETF | 500767355 | 3,374,500 | 84,463,735 | 64.15% |

| European Union Allowance (EUA) 2026 Note | US36255HES31 | 41,677,000 | 25,868,956 | 19.65% |

| Euro FX Futures | ECM6 Curncy | 130 | 18,826,438 | 14.3% |

| EURO | EUR | 5,994,970 | 6,907,444 | 5.25% |

| State Street Institutional U.S. Government Money Market Fund | GVMXX | 6,723,142 | 6,723,141 | 5.11% |

| BRITISH STERLING POUND | GBP | 2,427,360 | 3,200,971 | 2.43% |

| USD Cash & Equivalents** | USD | -14,254,356 | -14,254,356 | -10.83% |

| Total | 131,736,328 | 100% |

Carbon Allowance Futures Breakdown (Data as of 3/31/2026)

- EUA 2026 Note: 51.67%

- CCA 2026 Future: 26.62%

- EUA 2026 Future: 6.35%

- WCA 2026 Future: 5.90%

- RGGI 2026 Future: 5.66%

- UKA 2026 Future: 3.91%

Currency Exposure Breakdown (Data as of 3/31/2026)

- EUR: 58.84%

- USD: 38.78%

- GBP: 2.43%

Part II: Deep Dive into the Carbon Allowance Markets

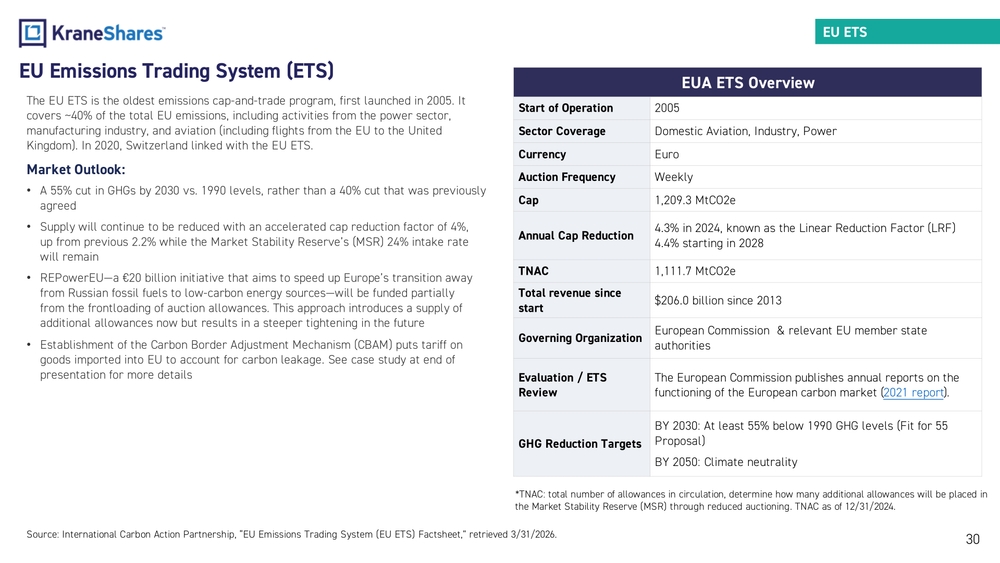

EU Emissions Trading System (ETS)

The EU ETS is the oldest emissions cap-and-trade program, first launched in 2005. It covers ~40% of the total EU emissions, including activities from the power sector, manufacturing industry, and aviation (including flights from the EU to the United Kingdom). In 2020, Switzerland linked with the EU ETS.

Market Outlook

- A 55% cut in GHGs by 2030 vs. 1990 levels, rather than a 40% cut that was previously agreed

- Supply will continue to be reduced with an accelerated cap reduction factor of 4%, up from previous 2.2% while the Market Stability Reserve's (MSR) 24% intake rate will remain

- REPowerEU—a €20 billion initiative that aims to speed up Europe's transition away from Russian fossil fuels to low-carbon energy sources—will be funded partially from the frontloading of auction allowances. This approach introduces a supply of additional allowances now but results in a steeper tightening in the future

- Establishment of the Carbon Border Adjustment Mechanism (CBAM) puts tariff on goods imported into EU to account for carbon leakage. See case study at end of presentation for more details

EUA ETS Overview

| Start of Operation | 2005 |

| Sector Coverage | Domestic Aviation, Industry, Power |

| Currency | Euro |

| Auction Frequency | Weekly |

| Cap | 1,209.3 MtCO2e |

| Annual Cap Reduction | 4.3% in 2024, known as the Linear Reduction Factor (LRF); 4.4% starting in 2028 |

| TNAC | 1,111.7 MtCO2e |

| Total revenue since start | $206.0 billion since 2013 |

| Governing Organization | European Commission & relevant EU member state authorities |

| Evaluation / ETS Review | The European Commission publishes annual reports on the functioning of the European carbon market (2021 report) |

| GHG Reduction Targets | BY 2030: At least 55% below 1990 GHG levels (Fit for 55 Proposal); BY 2050: Climate neutrality |