IVOL Presentation

by Kraneshares

IVOL: The Quadratic Interest Rate Volatility and Inflation Hedge ETF

Q1 2026

About Quadratic Capital Management and Krane Funds Advisors

Quadratic Capital Management

Quadratic Capital Management is an innovative asset management firm founded in 2013 by Nancy Davis. Quadratic utilizes its significant expertise in fixed income and options markets to construct The Quadratic Interest Rate Volatility and Inflation Hedge ETF (NYSE Ticker: IVOL). Quadratic Capital Management serves as the Investment Sub-Adviser to the IVOL ETF.

Krane Funds Advisors

Krane Funds was founded in 2013 by Jonathan Krane and manages approximately $12 billion. The firm seeks to provide innovative, first to market strategies that have been developed based on the firm and its partners' deep knowledge of investing. Krane Funds Advisors serves as the Investment Adviser to the IVOL ETF.

Select IVOL Awards and Designations

- Forbes profiles Nancy Davis and IVOL strategy

- Nancy named to the Inaugural List of Barron's 100 Most Influential Women in Finance

- IVOL named "Best New US Fixed Income Fund" by ETF.com*

- WSJ profiled Nancy Davis and IVOL in featured article

- IVOL designated for NAIC 1.C Capital Treatment as Schedule D Bond ETF

*For Best New US Fixed Income Fund of 2019 criteria please visit: www.etf.com/sections/features-and-news/2019-etfcom-award-winners/page/0/1

Quadratic Capital – Our Approach to Investing

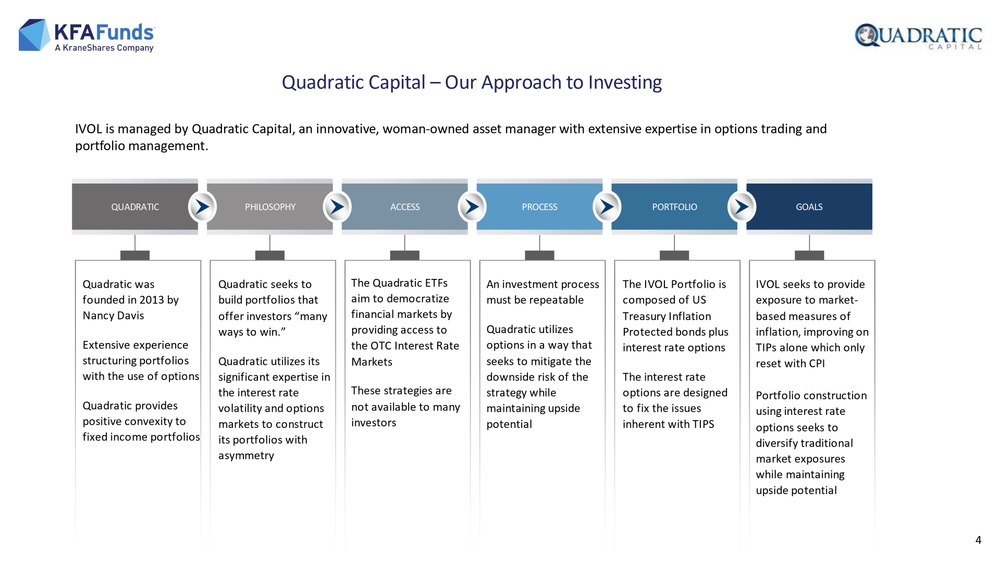

IVOL is managed by Quadratic Capital, an innovative, woman-owned asset manager with extensive expertise in options trading and portfolio management.

QUADRATIC

- Quadratic was founded in 2013 by Nancy Davis

- Extensive experience structuring portfolios with the use of options

- Quadratic provides positive convexity to fixed income portfolios

PHILOSOPHY

- Quadratic seeks to build portfolios that offer investors "many ways to win."

- Quadratic utilizes its significant expertise in the interest rate volatility and options markets to construct its portfolios with asymmetry

ACCESS

- The Quadratic ETFs aim to democratize financial markets by providing access to the OTC Interest Rate Markets

- These strategies are not available to many investors

PROCESS

- An investment process must be repeatable

- Quadratic utilizes options in a way that seeks to mitigate the downside risk of the strategy while maintaining upside potential

PORTFOLIO

- The IVOL Portfolio is composed of US Treasury Inflation Protected bonds plus interest rate options

- The interest rate options are designed to fix the issues inherent with TIPS

GOALS

- IVOL seeks to provide exposure to market-based measures of inflation, improving on TIPs alone which only reset with CPI

- Portfolio construction using interest rate options seeks to diversify traditional market exposures while maintaining upside potential

Access: IVOL Provides Exposure to the Rates Markets

➢ IVOL provides access to the OTC rates market, which is the largest single asset class; also provides the potential for differentiated performance from stocks and bonds. Until IVOL, this market was very difficult to access without ISDAs.

➢ IVOL's OTC rates options provide exposure to the shape of the interest rate yield curve, which is largely a result of inflation expectations. Thus, the options have the potential to increase in value with a normalization of inflation expectations.

Key features:

➢ Potential for enhanced, inflation-protected distributions. IVOL has distributed at least 30 bps per month for over 6 years in a row.

➢ IVOL's options are fully funded, so the maximum downside is known and limited to the market value of the options.

➢ Through its options, IVOL is long OTC fixed income volatility, providing potential profit from market stress as volatility increases.

➢ IVOL's options have the potential to benefit from relative interest rate moves – whether those moves are lower (or negative) rates in the front end and/or higher rates in the back end – the option payoffs are agnostic to the level of interest rates.

Relative Sizes of US Financial Markets

- OTC RATES: 55%

- Equities: 23%

- Credit: 13%

- Treasuries: 9%

Source: Nasdaq, SIFMA and BIS. "US OTC Rates" defined as the notional value outstanding in interest rate contracts denominated in USD as of H1 2025.

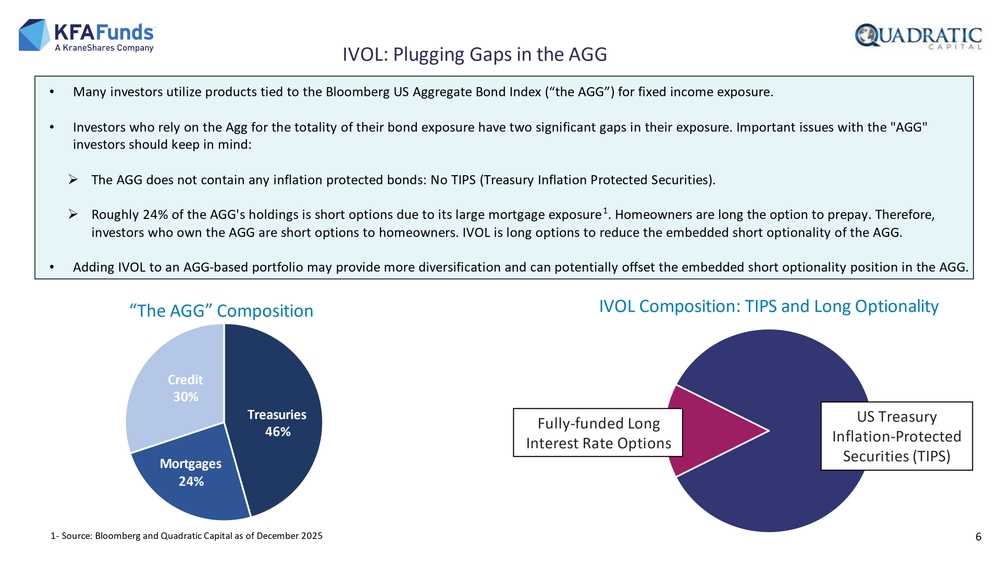

IVOL: Plugging Gaps in the AGG

-

Many investors utilize products tied to the Bloomberg US Aggregate Bond Index ("the AGG") for fixed income exposure.

-

Investors who rely on the Agg for the totality of their bond exposure have two significant gaps in their exposure. Important issues with the "AGG" investors should keep in mind:

➢ The AGG does not contain any inflation protected bonds: No TIPS (Treasury Inflation Protected Securities).

➢ Roughly 24% of the AGG's holdings is short options due to its large mortgage exposure¹. Homeowners are long the option to prepay. Therefore, investors who own the AGG are short options to homeowners. IVOL is long options to reduce the embedded short optionality of the AGG.

-

Adding IVOL to an AGG-based portfolio may provide more diversification and can potentially offset the embedded short optionality position in the AGG.

"The AGG" Composition

- Treasuries: 46%

- Mortgages: 24%

- Credit: 30%

IVOL Composition: TIPS and Long Optionality

- US Treasury Inflation-Protected Securities (TIPS)

- Fully-funded Long Interest Rate Options

¹- Source: Bloomberg and Quadratic Capital as of December 2025

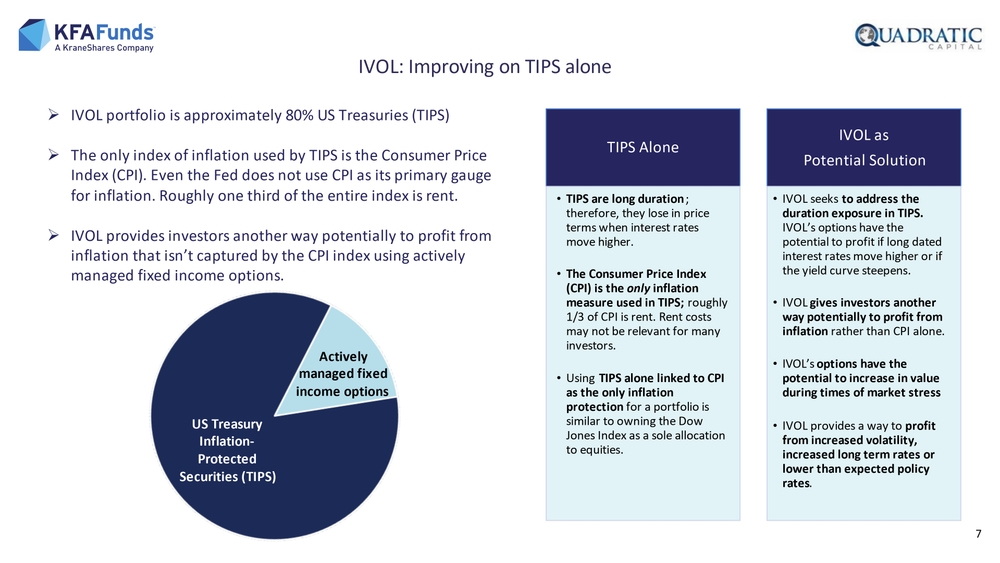

IVOL: Improving on TIPS alone

➢ IVOL portfolio is approximately 80% US Treasuries (TIPS)

➢ The only index of inflation used by TIPS is the Consumer Price Index (CPI). Even the Fed does not use CPI as its primary gauge for inflation. Roughly one third of the entire index is rent.

➢ IVOL provides investors another way potentially to profit from inflation that isn't captured by the CPI index using actively managed fixed income options.

TIPS Alone

- TIPS are long duration; therefore, they lose in price terms when interest rates move higher.

- The Consumer Price Index (CPI) is the only inflation measure used in TIPS; roughly 1/3 of CPI is rent. Rent costs may not be relevant for many investors.

- Using TIPS alone linked to CPI as the only inflation protection for a portfolio is similar to owning the Dow Jones Index as a sole allocation to equities.

IVOL as Potential Solution

- IVOL seeks to address the duration exposure in TIPS. IVOL's options have the potential to profit if long dated interest rates move higher or if the yield curve steepens.

- IVOL gives investors another way potentially to profit from inflation rather than CPI alone.

- IVOL's options have the potential to increase in value during times of market stress

- IVOL provides a way to profit from increased volatility, increased long term rates or lower than expected policy rates.

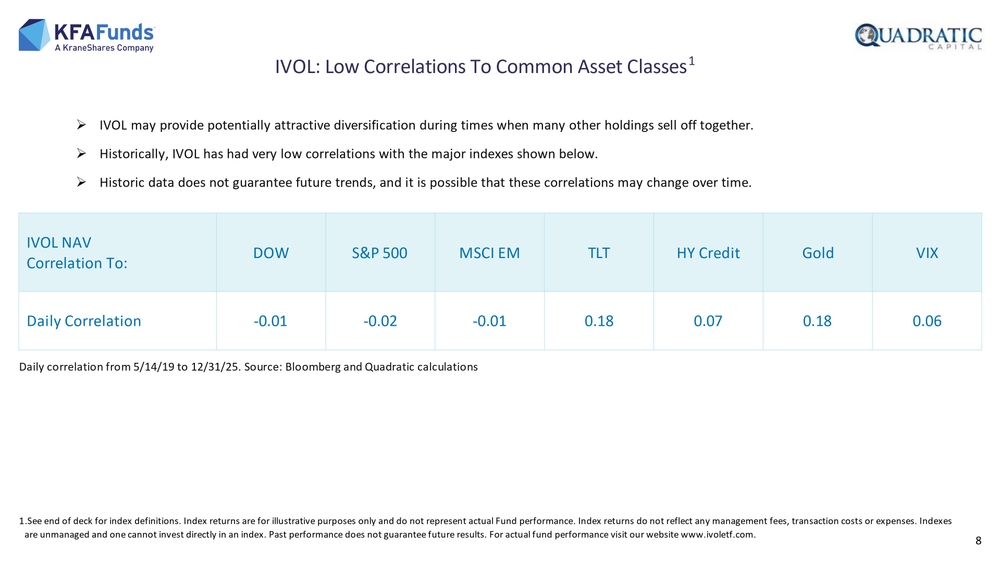

IVOL: Low Correlations To Common Asset Classes¹

➢ IVOL may provide potentially attractive diversification during times when many other holdings sell off together.

➢ Historically, IVOL has had very low correlations with the major indexes shown below.

➢ Historic data does not guarantee future trends, and it is possible that these correlations may change over time.

IVOL NAV Correlation To:

| Index | Daily Correlation |

|---|---|

| DOW | -0.01 |

| S&P 500 | -0.02 |

| MSCI EM | -0.01 |

| TLT | 0.18 |

| HY Credit | 0.07 |

| Gold | 0.18 |

| VIX | 0.06 |

Daily correlation from 5/14/19 to 12/31/25. Source: Bloomberg and Quadratic calculations

¹See end of deck for index definitions. Index returns are for illustrative purposes only and do not represent actual Fund performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results. For actual fund performance visit our website www.ivoletf.com.

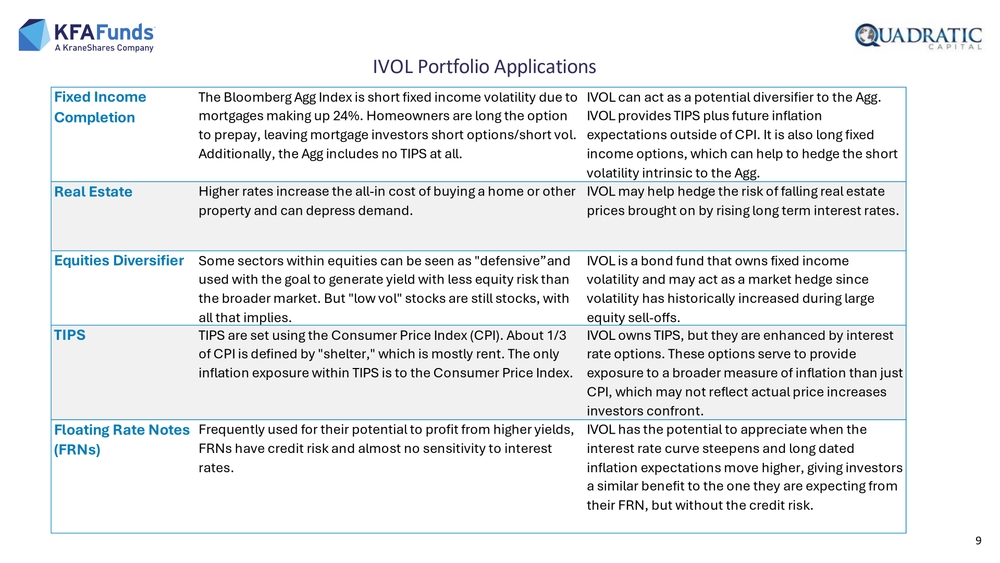

IVOL Portfolio Applications

Fixed Income Completion

The Bloomberg Agg Index is short fixed income volatility due to mortgages making up 24%. Homeowners are long the option to prepay, leaving mortgage investors short options/short vol. Additionally, the Agg includes no TIPS at all.

IVOL can act as a potential diversifier to the Agg. IVOL provides TIPS plus future inflation expectations outside of CPI. It is also long fixed income options, which can help to hedge the short volatility intrinsic to the Agg.

Real Estate

Higher rates increase the all-in cost of buying a home or other property and can depress demand.

IVOL may help hedge the risk of falling real estate prices brought on by rising long term interest rates.

Equities Diversifier

Some sectors within equities can be seen as "defensive"and used with the goal to generate yield with less equity risk than the broader market. But "low vol" stocks are still stocks, with all that implies.

IVOL is a bond fund that owns fixed income volatility and may act as a market hedge since volatility has historically increased during large equity sell-offs.

TIPS

TIPS are set using the Consumer Price Index (CPI). About 1/3 of CPI is defined by "shelter," which is mostly rent. The only inflation exposure within TIPS is to the Consumer Price Index.

IVOL owns TIPS, but they are enhanced by interest rate options. These options serve to provide exposure to a broader measure of inflation than just CPI, which may not reflect actual price increases investors confront.

Floating Rate Notes (FRNs)

Frequently used for their potential to profit from higher yields, FRNs have credit risk and almost no sensitivity to interest rates.

IVOL has the potential to appreciate when the interest rate curve steepens and long dated inflation expectations move higher, giving investors a similar benefit to the one they are expecting from their FRN, but without the credit risk.

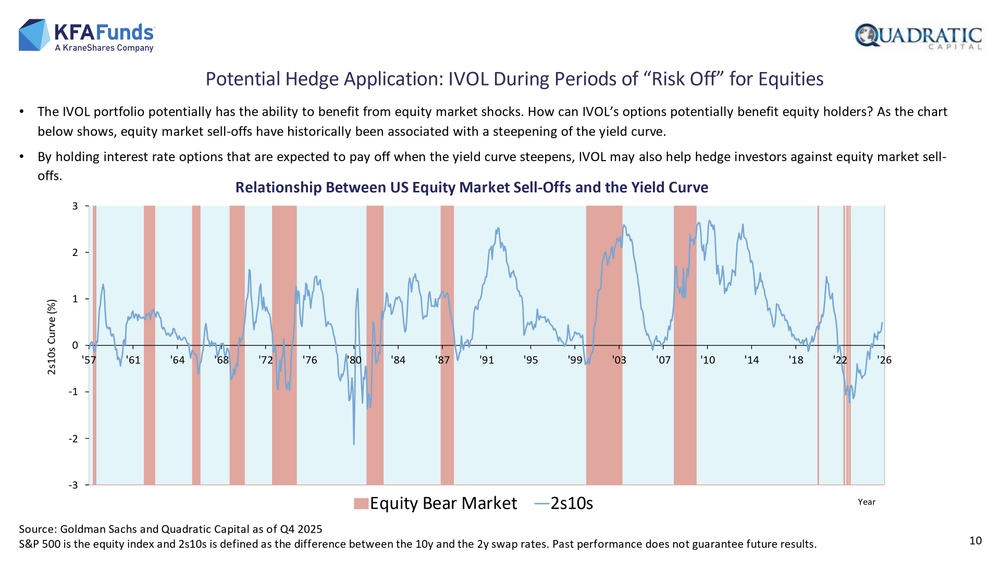

Potential Hedge Application: IVOL During Periods of "Risk Off" for Equities

-

The IVOL portfolio potentially has the ability to benefit from equity market shocks. How can IVOL's options potentially benefit equity holders? As the chart below shows, equity market sell-offs have historically been associated with a steepening of the yield curve.

-

By holding interest rate options that are expected to pay off when the yield curve steepens, IVOL may also help hedge investors against equity market sell-offs.

Relationship Between US Equity Market Sell-Offs and the Yield Curve

[Chart showing the relationship between Equity Bear Markets and the 2s10s yield curve from 1957 to 2026]

Source: Goldman Sachs and Quadratic Capital as of Q4 2025 S&P 500 is the equity index and 2s10s is defined as the difference between the 10y and the 2y swap rates. Past performance does not guarantee future results.

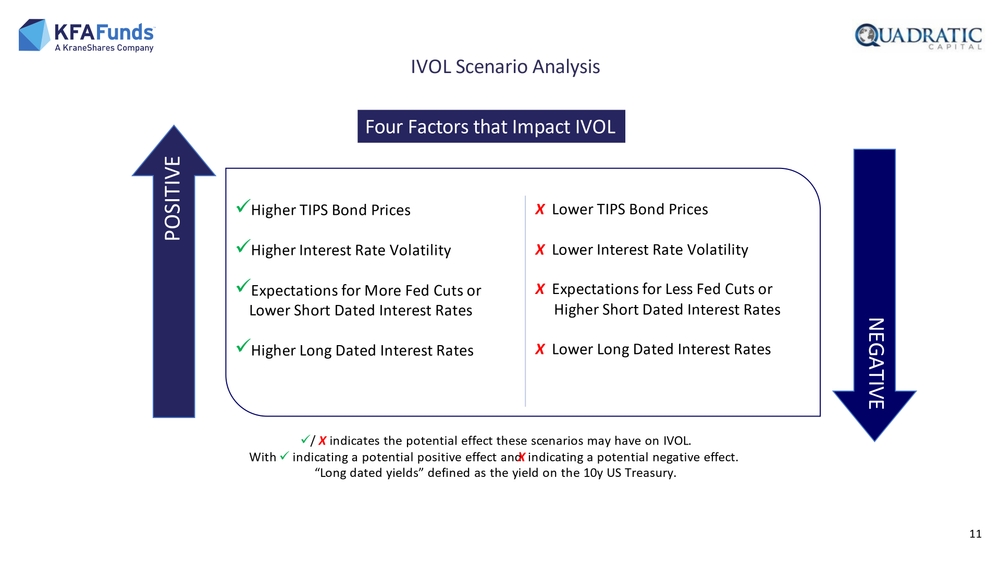

IVOL Scenario Analysis

Four Factors that Impact IVOL

POSITIVE

✓ Higher TIPS Bond Prices ✓ Higher Interest Rate Volatility ✓ Expectations for More Fed Cuts or Lower Short Dated Interest Rates ✓ Higher Long Dated Interest Rates

NEGATIVE

X Lower TIPS Bond Prices X Lower Interest Rate Volatility X Expectations for Less Fed Cuts or Higher Short Dated Interest Rates X Lower Long Dated Interest Rates

✓/ X indicates the potential effect these scenarios may have on IVOL. With ✓ indicating a potential positive effect and X indicating a potential negative effect. "Long dated yields" defined as the yield on the 10y US Treasury.

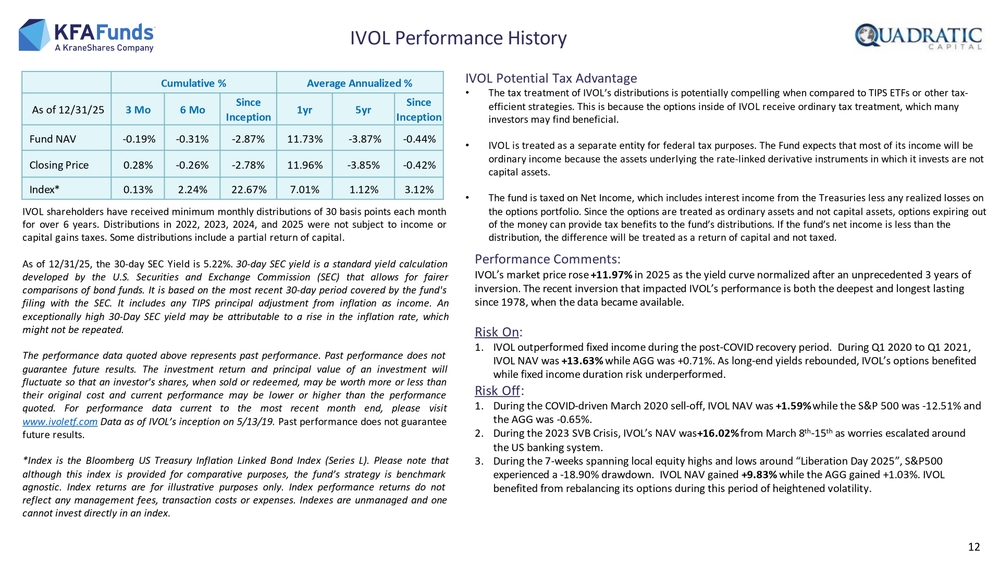

IVOL Performance History

IVOL Potential Tax Advantage

- The tax treatment of IVOL's distributions is potentially compelling when compared to TIPS ETFs or other tax-efficient strategies. This is because the options inside of IVOL receive ordinary tax treatment, which many investors may find beneficial.

- IVOL is treated as a separate entity for federal tax purposes. The Fund expects that most of its income will be ordinary income because the assets underlying the rate-linked derivative instruments in which it invests are not capital assets.

- The fund is taxed on Net Income, which includes interest income from the Treasuries less any realized losses on the options portfolio. Since the options are treated as ordinary assets and not capital assets, options expiring out of the money can provide tax benefits to the fund's distributions. If the fund's net income is less than the distribution, the difference will be treated as a return of capital and not taxed.

Performance Comments:

IVOL's market price rose +11.97% in 2025 as the yield curve normalized after an unprecedented 3 years of inversion. The recent inversion that impacted IVOL's performance is both the deepest and longest lasting since 1978, when the data became available.

Risk On:

- IVOL outperformed fixed income during the post-COVID recovery period. During Q1 2020 to Q1 2021, IVOL NAV was +13.63% while AGG was +0.71%. As long-end yields rebounded, IVOL's options benefited while fixed income duration risk underperformed.

Risk Off:

- During the COVID-driven March 2020 sell-off, IVOL NAV was +1.59% while the S&P 500 was -12.51% and the AGG was -0.65%.

- During the 2023 SVB Crisis, IVOL's NAV was +16.02% from March 8th-15th as worries escalated around the US banking system.

- During the 7-weeks spanning local equity highs and lows around "Liberation Day 2025", S&P500 experienced a -18.90% drawdown. IVOL NAV gained +9.83% while the AGG gained +1.03%. IVOL benefited from rebalancing its options during this period of heightened volatility.

IVOL shareholders have received minimum monthly distributions of 30 basis points each month for over 6 years. Distributions in 2022, 2023, 2024, and 2025 were not subject to income or capital gains taxes. Some distributions include a partial return of capital.

As of 12/31/25, the 30-day SEC Yield is 5.22%. 30-day SEC yield is a standard yield calculation developed by the U.S. Securities and Exchange Commission (SEC) that allows for fairer comparisons of bond funds. It is based on the most recent 30-day period covered by the fund's filing with the SEC. It includes any TIPS principal adjustment from inflation as income. An exceptionally high 30-Day SEC yield may be attributable to a rise in the inflation rate, which might not be repeated.

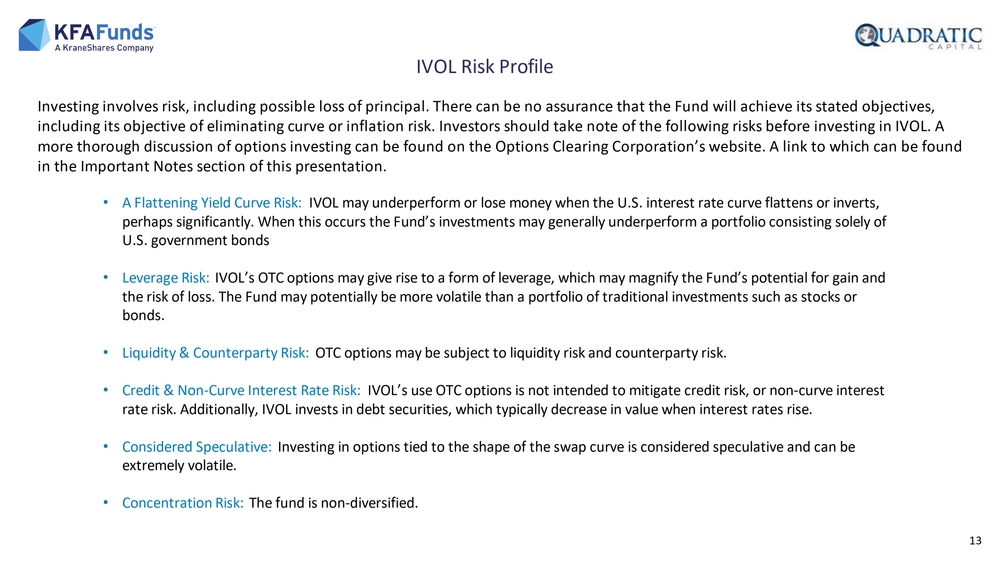

IVOL Risk Profile

Investing involves risk, including possible loss of principal. There can be no assurance that the Fund will achieve its stated objectives, including its objective of eliminating curve or inflation risk. Investors should take note of the following risks before investing in IVOL. A more thorough discussion of options investing can be found on the Options Clearing Corporation's website. A link to which can be found in the Important Notes section of this presentation.

-

A Flattening Yield Curve Risk: IVOL may underperform or lose money when the U.S. interest rate curve flattens or inverts, perhaps significantly. When this occurs the Fund's investments may generally underperform a portfolio consisting solely of U.S. government bonds

-

Leverage Risk: IVOL's OTC options may give rise to a form of leverage, which may magnify the Fund's potential for gain and the risk of loss. The Fund may potentially be more volatile than a portfolio of traditional investments such as stocks or bonds.

-

Liquidity & Counterparty Risk: OTC options may be subject to liquidity risk and counterparty risk.

-

Credit & Non-Curve Interest Rate Risk: IVOL's use OTC options is not intended to mitigate credit risk, or non-curve interest rate risk. Additionally, IVOL invests in debt securities, which typically decrease in value when interest rates rise.

-

Considered Speculative: Investing in options tied to the shape of the swap curve is considered speculative and can be extremely volatile.

-

Concentration Risk: The fund is non-diversified.

Guide to Trading ETFs

ETF liquidity is determined by the asset class, not by the fund size

- Exchange-traded funds (ETFs) are a wrapper, and although an investor may hold a large percentage of an ETF, one must look at the percentage owned of the underlying asset class.

ETF investors are not impacted by other investors' trades in the same ETF

- The ETF structure is unique in that all investors transact independently on an exchange. Being a large or small owner in a fund does not cause one investor to be more or less impacted by the actions of other investors. In a mutual fund, all investors are impacted by the trading activity of other holders in the fund.

An ETF closure does not create principal risk

- If a fund were to close, neither large nor small investors would have a principal risk. The fund would be liquidated by the portfolio manager, and the investors would receive back NAV of the fund, minus costs, at the time of liquidation.

Trading in and out and fund size

- Investors can trade in and out of a fund regardless of the fund's AUM. ETF liquidity providers (market makers) can easily transfer the liquidity of the underlying basket into ETF shares. Market makers also accept NAV based orders for larger tickets.

Understanding ETF Liquidity

An ETF is not a stock

- If an ETF does not trade a certain number of shares per day, is the fund illiquid? No. It's a plausible assumption from a single-stock perspective, but with ETFs, there is more to consider. The key is the difference between the primary and secondary market liquidity of an ETF.

Primary Market vs. Secondary Market

-

Most noninstitutional investors transact in the secondary market—which means investors are trading the ETF shares that currently exist. Secondary liquidity is the "on screen" liquidity you see from your brokerage (e.g., volume and spreads), and it's determined primarily by the volume of ETF shares traded.

-

However, one of the key features of ETFs is that the supply of shares is flexible—shares can be "created" or "redeemed" to offset changes in demand. Primary liquidity is concerned with how efficient it is to create or redeem shares. Liquidity in one market is not indicative of liquidity in the other market.

-

The determinants of primary market liquidity are different than the determinants of secondary market liquidity. In the secondary market, liquidity is primarily a function of the value of the ETF shares traded and the frequency and volume of the trading of those shares throughout the trading day. When placing a large trade—on the scale of tens of thousands of shares—investors are sometimes able to circumvent an illiquid secondary market by using an "authorized participant" (AP) to reach through to the primary market to "create" new ETF shares at NAV price.

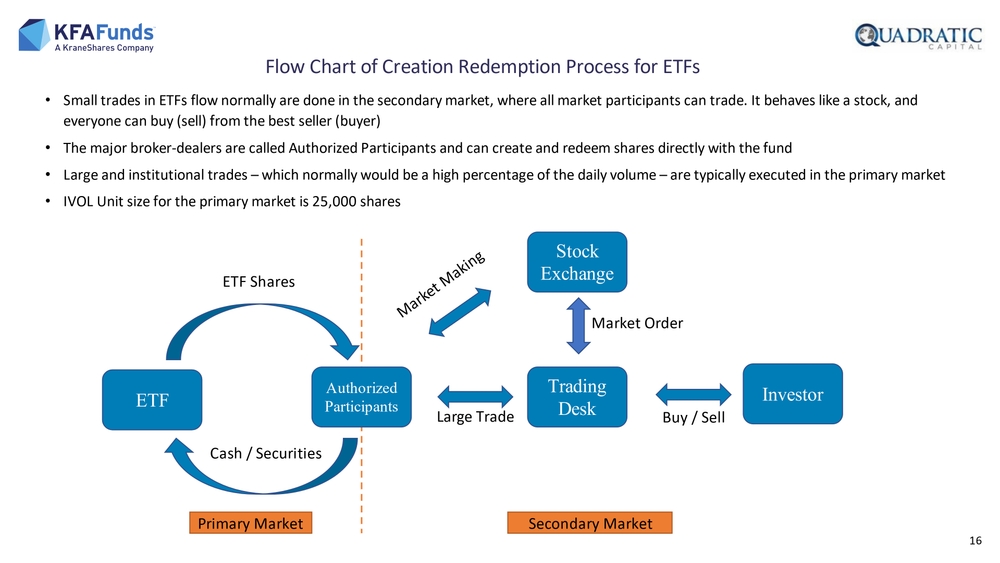

Flow Chart of Creation Redemption Process for ETFs

-

Small trades in ETFs flow normally are done in the secondary market, where all market participants can trade. It behaves like a stock, and everyone can buy (sell) from the best seller (buyer)

-

The major broker-dealers are called Authorized Participants and can create and redeem shares directly with the fund

-

Large and institutional trades – which normally would be a high percentage of the daily volume – are typically executed in the primary market

-

IVOL Unit size for the primary market is 25,000 shares

[The image shows a flow chart illustrating the ETF creation/redemption process, with Primary Market on the left (showing ETF and Authorized Participants exchanging ETF Shares and Cash/Securities) and Secondary Market on the right (showing Trading Desk, Stock Exchange, and Investor interactions through Market Orders and Buy/Sell activities)]

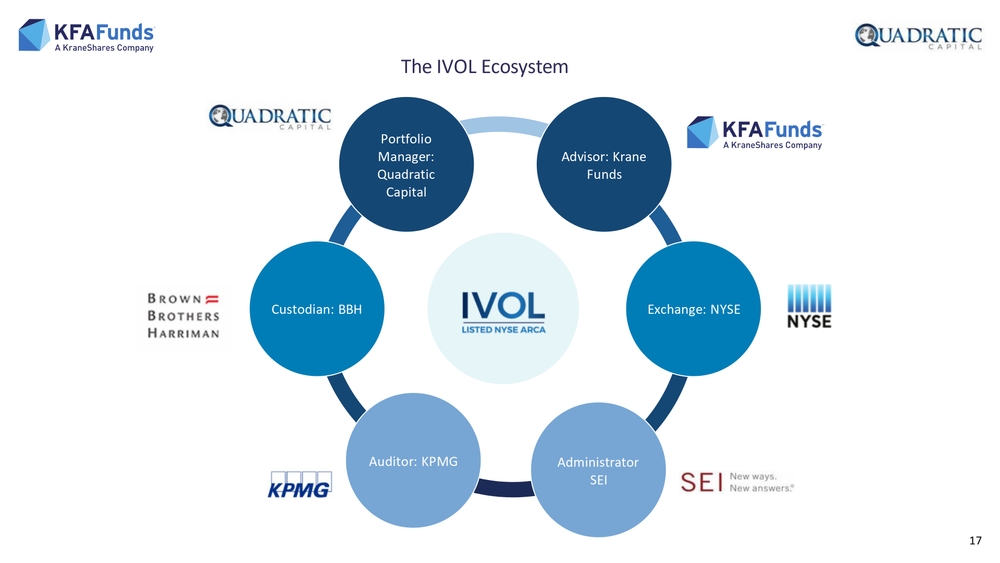

The IVOL Ecosystem

[The image shows a circular diagram illustrating the IVOL ecosystem with the following key participants:]

- Portfolio Manager: Quadratic Capital

- Advisor: Krane Funds

- Exchange: NYSE

- Administrator: SEI

- Auditor: KPMG

- Custodian: BBH

Portfolio Management and Capital Markets Leadership

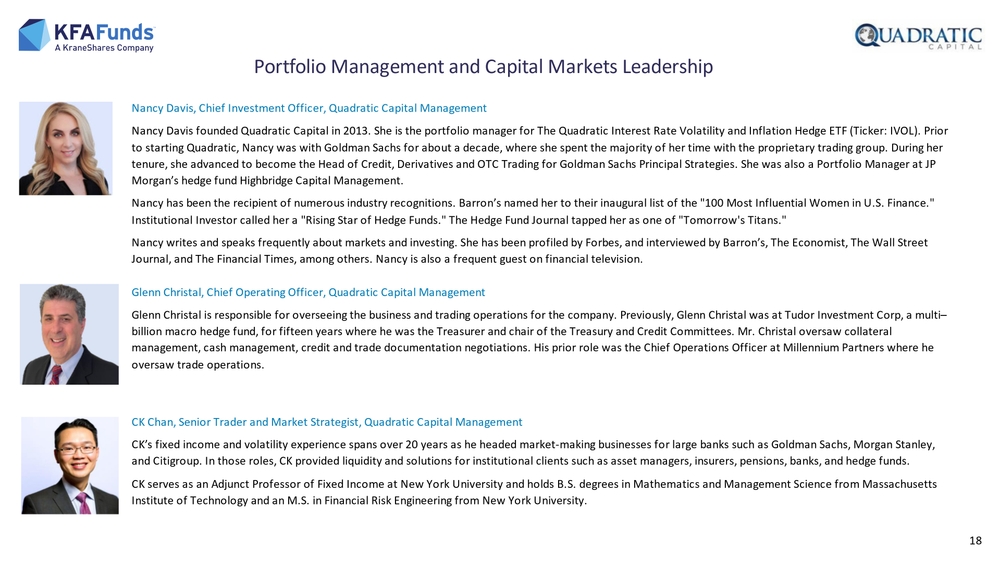

Nancy Davis, Chief Investment Officer, Quadratic Capital Management

Nancy Davis founded Quadratic Capital in 2013. She is the portfolio manager for The Quadratic Interest Rate Volatility and Inflation Hedge ETF (Ticker: IVOL). Prior to starting Quadratic, Nancy was with Goldman Sachs for about a decade, where she spent the majority of her time with the proprietary trading group. During her tenure, she advanced to become the Head of Credit, Derivatives and OTC Trading for Goldman Sachs Principal Strategies. She was also a Portfolio Manager at JP Morgan's hedge fund Highbridge Capital Management.

Nancy has been the recipient of numerous industry recognitions. Barron's named her to their inaugural list of the "100 Most Influential Women in U.S. Finance." Institutional Investor called her a "Rising Star of Hedge Funds." The Hedge Fund Journal tapped her as one of "Tomorrow's Titans."

Nancy writes and speaks frequently about markets and investing. She has been profiled by Forbes, and interviewed by Barron's, The Economist, The Wall Street Journal, and The Financial Times, among others. Nancy is also a frequent guest on financial television.

Glenn Christal, Chief Operating Officer, Quadratic Capital Management

Glenn Christal is responsible for overseeing the business and trading operations for the company. Previously, Glenn Christal was at Tudor Investment Corp, a multi–billion macro hedge fund, for fifteen years where he was the Treasurer and chair of the Treasury and Credit Committees. Mr. Christal oversaw collateral management, cash management, credit and trade documentation negotiations. His prior role was the Chief Operations Officer at Millennium Partners where he oversaw trade operations.

CK Chan, Senior Trader and Market Strategist, Quadratic Capital Management

CK's fixed income and volatility experience spans over 20 years as he headed market-making businesses for large banks such as Goldman Sachs, Morgan Stanley, and Citigroup. In those roles, CK provided liquidity and solutions for institutional clients such as asset managers, insurers, pensions, banks, and hedge funds. CK serves as an Adjunct Professor of Fixed Income at New York University and holds B.S. degrees in Mathematics and Management Science from Massachusetts Institute of Technology and an M.S. in Financial Risk Engineering from New York University.

Quadratic Capital and Krane Funds Leadership

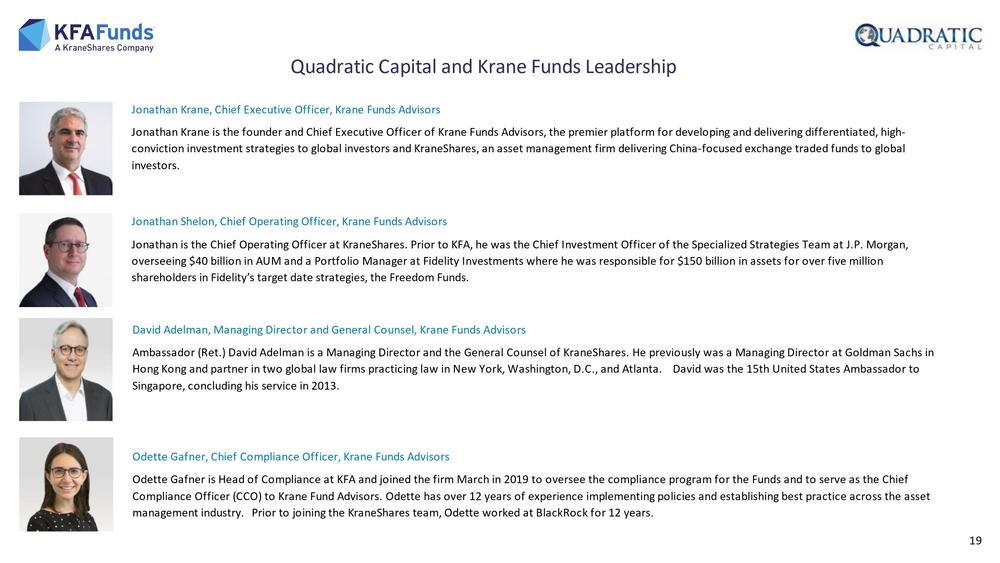

Jonathan Krane, Chief Executive Officer, Krane Funds Advisors

Jonathan Krane is the founder and Chief Executive Officer of Krane Funds Advisors, the premier platform for developing and delivering differentiated, high-conviction investment strategies to global investors and KraneShares, an asset management firm delivering China-focused exchange traded funds to global investors.

Jonathan Shelon, Chief Operating Officer, Krane Funds Advisors

Jonathan is the Chief Operating Officer at KraneShares. Prior to KFA, he was the Chief Investment Officer of the Specialized Strategies Team at J.P. Morgan, overseeing $40 billion in AUM and a Portfolio Manager at Fidelity Investments where he was responsible for $150 billion in assets for over five million shareholders in Fidelity's target date strategies, the Freedom Funds.

David Adelman, Managing Director and General Counsel, Krane Funds Advisors

Ambassador (Ret.) David Adelman is a Managing Director and the General Counsel of KraneShares. He previously was a Managing Director at Goldman Sachs in Hong Kong and partner in two global law firms practicing law in New York, Washington, D.C., and Atlanta. David was the 15th United States Ambassador to Singapore, concluding his service in 2013.

Odette Gafner, Chief Compliance Officer, Krane Funds Advisors

Odette Gafner is Head of Compliance at KFA and joined the firm March in 2019 to oversee the compliance program for the Funds and to serve as the Chief Compliance Officer (CCO) to Krane Fund Advisors. Odette has over 12 years of experience implementing policies and establishing best practice across the asset management industry. Prior to joining the KraneShares team, Odette worked at BlackRock for 12 years.

Quadratic Capital and Krane Funds Leadership

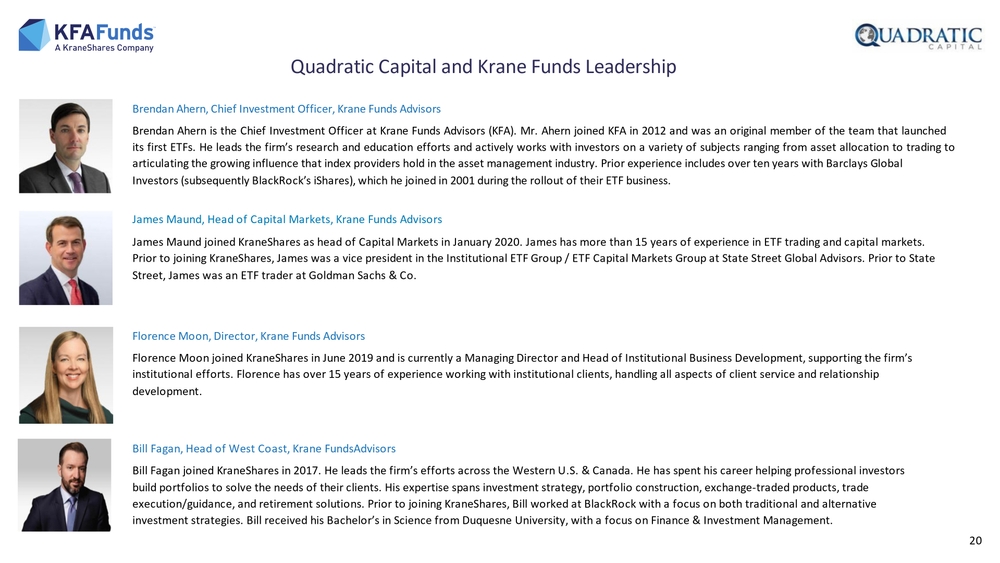

Brendan Ahern, Chief Investment Officer, Krane Funds Advisors

Brendan Ahern is the Chief Investment Officer at Krane Funds Advisors (KFA). Mr. Ahern joined KFA in 2012 and was an original member of the team that launched its first ETFs. He leads the firm's research and education efforts and actively works with investors on a variety of subjects ranging from asset allocation to trading to articulating the growing influence that index providers hold in the asset management industry. Prior experience includes over ten years with Barclays Global Investors (subsequently BlackRock's iShares), which he joined in 2001 during the rollout of their ETF business.

James Maund, Head of Capital Markets, Krane Funds Advisors

James Maund joined KraneShares as head of Capital Markets in January 2020. James has more than 15 years of experience in ETF trading and capital markets. Prior to joining KraneShares, James was a vice president in the Institutional ETF Group / ETF Capital Markets Group at State Street Global Advisors. Prior to State Street, James was an ETF trader at Goldman Sachs & Co.

Florence Moon, Director, Krane Funds Advisors

Florence Moon joined KraneShares in June 2019 and is currently a Managing Director and Head of Institutional Business Development, supporting the firm's institutional efforts. Florence has over 15 years of experience working with institutional clients, handling all aspects of client service and relationship development.

Bill Fagan, Head of West Coast, Krane Funds Advisors

Bill Fagan joined KraneShares in 2017. He leads the firm's efforts across the Western U.S. & Canada. He has spent his career helping professional investors build portfolios to solve the needs of their clients. His expertise spans investment strategy, portfolio construction, exchange-traded products, trade execution/guidance, and retirement solutions. Prior to joining KraneShares, Bill worked at BlackRock with a focus on both traditional and alternative investment strategies. Bill received his Bachelor's in Science from Duquesne University, with a focus on Finance & Investment Management.

Quadratic Capital and Krane Funds Leadership

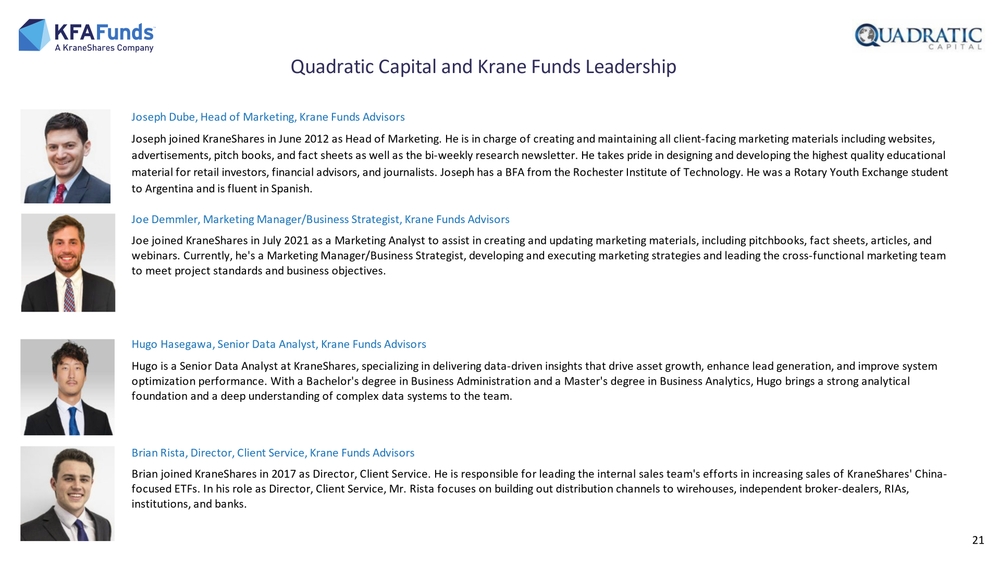

Joseph Dube, Head of Marketing, Krane Funds Advisors

Joseph joined KraneShares in June 2012 as Head of Marketing. He is in charge of creating and maintaining all client-facing marketing materials including websites, advertisements, pitch books, and fact sheets as well as the bi-weekly research newsletter. He takes pride in designing and developing the highest quality educational material for retail investors, financial advisors, and journalists. Joseph has a BFA from the Rochester Institute of Technology. He was a Rotary Youth Exchange student to Argentina and is fluent in Spanish.

Joe Demmler, Marketing Manager/Business Strategist, Krane Funds Advisors

Joe joined KraneShares in July 2021 as a Marketing Analyst to assist in creating and updating marketing materials, including pitchbooks, fact sheets, articles, and webinars. Currently, he's a Marketing Manager/Business Strategist, developing and executing marketing strategies and leading the cross-functional marketing team to meet project standards and business objectives.

Hugo Hasegawa, Senior Data Analyst, Krane Funds Advisors

Hugo is a Senior Data Analyst at KraneShares, specializing in delivering data-driven insights that drive asset growth, enhance lead generation, and improve system optimization performance. With a Bachelor's degree in Business Administration and a Master's degree in Business Analytics, Hugo brings a strong analytical foundation and a deep understanding of complex data systems to the team.

Brian Rista, Director, Client Service, Krane Funds Advisors

Brian joined KraneShares in 2017 as Director, Client Service. He is responsible for leading the internal sales team's efforts in increasing sales of KraneShares' China-focused ETFs. In his role as Director, Client Service, Mr. Rista focuses on building out distribution channels to wirehouses, independent broker-dealers, RIAs, institutions, and banks.

Quadratic Capital and Krane Funds Leadership

Zach Parke, Vice President, Client Services, Krane Funds Advisors

Zach joined KraneShares in March 2018 to further support the firm's Business Development efforts. His responsibilities include developing and fostering new relationships within Wirehouses, RIA Channels, Institutions, and Independent Broker-Dealers to promote and raise awareness of KraneShares as the thought-leader of China. Prior to joining the KraneShares team, Zach has worked with several asset management firms where he was engaged in educating and servicing financial advisors and their clients across various asset classes and products. Zach received his Bachelor of Business Administration in Finance with a concentration in Economics at the University of Delaware.

Kaitlyn Arico, Vice President, Client Services, Krane Funds Advisors

Kaitlyn joined KraneShares in March 2018 to further support the firm's Business Development efforts. As an Associate, Client Service, she focuses on cultivating new relationships with financial advisors, educating investors on China's investable markets and presenting KraneShares China-focused ETFs within the Wirehouses, RIA channels, Independent Brokers-Dealers and Institutions. Prior to KraneShares, Kaitlyn held positions as an Internal Sales Director and Regional Sales Director, representing a handful of different boutique asset managers across various asset classes. Kaitlyn received her BA in Business Economics from the State University of New York at Oneonta, with a concentration in Finance.

Brooke Farley, Business Development, Quadratic Capital Management

Brooke Farley joined Quadratic in 2018. Previously, she was a consultant for McKinsey & Company and a risk underwriter at Bond Investors Guaranty. Ms. Farley received her BA in Art History from Manhattanville College and received a Master of International Affairs (MIA) from Columbia University's School of International and Public Affairs. Ms. Farley holds her Series 7 and Series 63 Securities licenses.

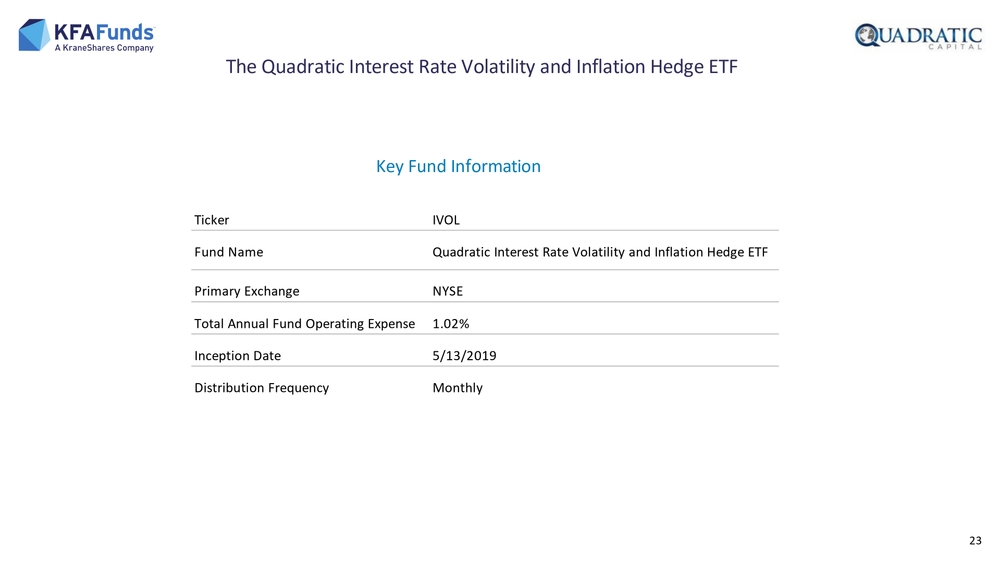

The Quadratic Interest Rate Volatility and Inflation Hedge ETF

Key Fund Information

| Ticker | IVOL |

|---|---|

| Fund Name | Quadratic Interest Rate Volatility and Inflation Hedge ETF |

| Primary Exchange | NYSE |

| Total Annual Fund Operating Expense | 1.02% |

| Inception Date | 5/13/2019 |

| Distribution Frequency | Monthly |

Index Definitions

The Dow Jones Industrial Average ("Dow") is an index that tracks 30 large, publicly-owned companies trading on the New York Stock Exchange and the NASDAQ.

The S&P 500, ("S&P"), is a stock market index that measures the stock performance of 500 large companies listed on stock exchanges in the US.

The MSCI Emerging Markets ("MSCI EM") Index captures large and mid cap representation across 26 Emerging Markets (EM) countries.

The iShares 20+ Year Treasury ("TLT") ETF seeks to track the investment results of an index composed of US Treasury bonds with remaining maturities greater than twenty years.

The iBoxx iShares High Yield Corporate Bond Index ("HY Credit") is designed to reflect the performance of USD denominated high yield corporate debt.

VIX is a CBOE index that represents equity volatility of 30-day expectations of the S&P 500 equity index.

Bloomberg US Aggregate Bond Index ("Agg") is a broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS and CMBS (agency and non-agency).

Bloomberg US Treasury Inflation Linked Bond Index (Series L) measures the performance of the US Treasury Inflation Protected Securities (TIPS) market.

Important Notes

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please visit www.IVOLETF.com.

ETF shares are not redeemable with the issuing fund other than in large transactions with institutional investors. Shares of any ETF are generally bought and sold at market price (not NAV). Market price returns are based on the official closing price of an ETF share or, if the official closing price isn't available, the midpoint between the national best bid and national best offer ("NBBO") as of the time the ETF calculates current NAV per share. NAVs are calculated using prices as of 4:00 PM Eastern Time. The returns shown do not represent the returns you would receive if you bought and sold shares at other times. Any brokerage commissions will reduce returns.

There is no guarantee the Fund will declare distributions in the future or that, if declared, such distributions will remain at current levels or increase over time.

Investing involves risk, including possible loss of principal. There can be no assurance that a Fund will achieve its stated investment objectives. The Fund does not seek to mitigate credit risk, non-curve interest rate risk, or other factors influencing the price of U.S. government bonds, which factors may have a greater impact on the bonds' returns than the U.S. interest rate curve or inflation. There is no guarantee that the Fund's investments will eliminate or mitigate curve risk, or inflation risk on long positions in U.S. government bonds. In addition, when the forward U.S. interest rate curve flattens, the Fund's investments will generally underperform a portfolio comprised solely of the U.S. government bonds. In a flattening curve environment (a reduction in the spread between shorter and longer term interest rates), the Fund's strategy could result in disproportionately larger losses in the Fund's options as compared to gains or losses in the U.S. government bond positions. The Fund's exposure to options subjects the Fund to greater volatility than investments in traditional securities and may magnify the Funds' gains or losses. The Fund is non-diversified and therefore has concentration risk.

OTC options generally have more flexible terms negotiated between the buyer and the seller. As a result, such instruments generally are subject to greater counterparty risk. OTC instruments also may be subject to greater liquidity risk. There are risks involved with investing in options including the potential loss of the amount, or premium paid for the option.

This material must be preceded or accompanied by a current prospectus. Investors should read it carefully before investing or sending money.

IVOL is distributed by SEI Investments Distribution Co. (SIDCO), 1 Freedom Valley Drive, Oaks, PA 19456. The Fund's sub-adviser is Quadratic Capital Management LLC (Quadratic). The Fund's advisor is Krane Fund Advisors LLC (Krane). SIDCO is not affiliated with Quadratic or Krane. Neither Quadratic, Krane nor SIDCO or their affiliates provide tax advice. Please note that (i) any discussion of U.S. tax matters contained in this communication cannot be used by you for the purpose of avoiding tax penalties; (ii) this communication was written to support the promotion or marketing of the matters addressed herein; and (iii) you should seek advice based on your particular circumstances from an independent tax advisor.