China ETF | KURE : Exposure to China’s Health Care Tech

by Kraneshares

China Healthcare: Potential Opportunities From One Of The Fastest Growing Major Global Healthcare Markets

An Overview of the KraneShares MSCI All China Healthcare Index ETF (Ticker: KURE)

Based on the expected growth rate of health spending in China using data as of 12/31/2024 from the Pew Research Center and OECD, and compiled by KraneShares.

Introduction to KraneShares

About KraneShares

Krane Funds Advisors, LLC is a specialist investment manager focused on China, Climate, and Alternative assets. KraneShares seeks to provide innovative, high conviction, and first to market strategies. The firm was founded in 2013 and manages for institutions and individuals globally. The firm is a signatory of the United Nations-supported Principles for Responsible Investment (UN PRI).

Sign up to our daily (or weekly) note on China's capital markets: www.chinalastnight.com

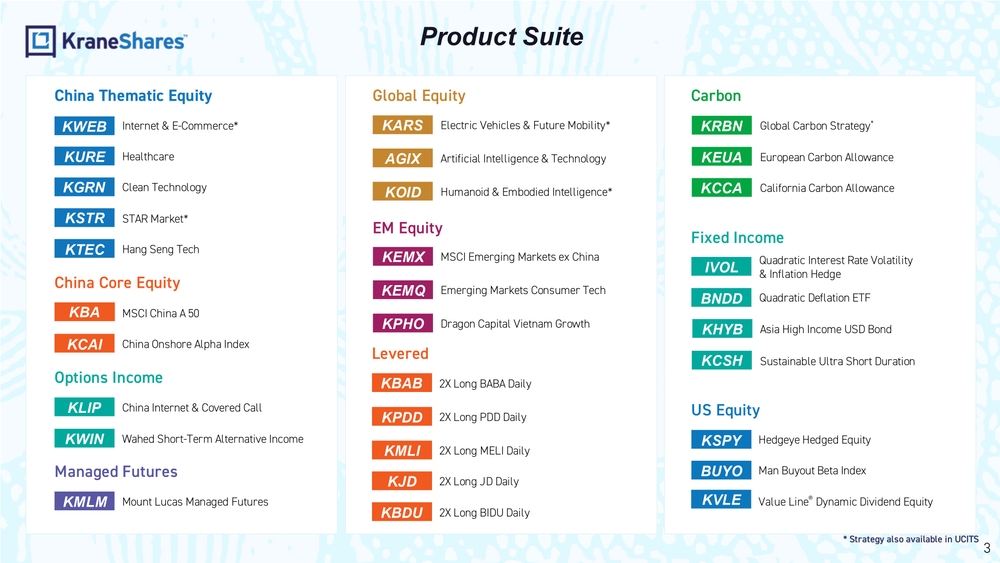

Product Suite

China Thematic Equity

- KWEB: Internet & E-Commerce*

- KURE: Healthcare

- KGRN: Clean Technology

- KSTR: STAR Market*

- KTEC: Hang Seng Tech

China Core Equity

- KBA: MSCI China A 50

- KCAI: China Onshore Alpha Index

Options Income

- KLIP: China Internet & Covered Call

- KWIN: Wahed Short-Term Alternative Income

Managed Futures

- KMLM: Mount Lucas Managed Futures

Global Equity

- KARS: Electric Vehicles & Future Mobility*

- AGIX: Artificial Intelligence & Technology

- KOID: Humanoid & Embodied Intelligence*

EM Equity

- KEMX: MSCI Emerging Markets ex China

- KEMQ: Emerging Markets Consumer Tech

- KPHO: Dragon Capital Vietnam Growth

Levered

- KBAB: 2X Long BABA Daily

- KPDD: 2X Long PDD Daily

- KMLI: 2X Long MELI Daily

- KJD: 2X Long JD Daily

- KBDU: 2X Long BIDU Daily

Carbon

- KRBN: Global Carbon Strategy*

- KEUA: European Carbon Allowance

- KCCA: California Carbon Allowance

Fixed Income

- IVOL: Quadratic Interest Rate Volatility & Inflation Hedge

- BNDD: Quadratic Deflation ETF

- KHYB: Asia High Income USD Bond

- KCSH: Sustainable Ultra Short Duration

US Equity

- KSPY: Hedgeye Hedged Equity

- BUYO: Man Buyout Beta Index

- KVLE: Value Line® Dynamic Dividend Equity

*Strategy also available in UCITS

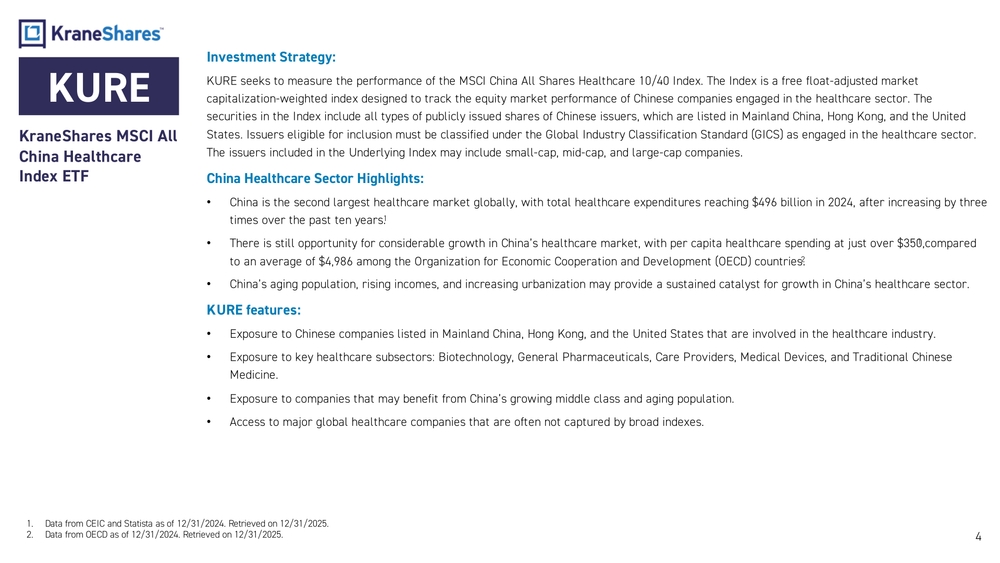

KraneShares MSCI All China Healthcare Index ETF (KURE)

Investment Strategy:

KURE seeks to measure the performance of the MSCI China All Shares Healthcare 10/40 Index. The Index is a free float-adjusted market capitalization-weighted index designed to track the equity market performance of Chinese companies engaged in the healthcare sector. The securities in the Index include all types of publicly issued shares of Chinese issuers, which are listed in Mainland China, Hong Kong, and the United States. Issuers eligible for inclusion must be classified under the Global Industry Classification Standard (GICS) as engaged in the healthcare sector. The issuers included in the Underlying Index may include small-cap, mid-cap, and large-cap companies.

China Healthcare Sector Highlights:

- China is the second largest healthcare market globally, with total healthcare expenditures reaching $496 billion in 2024, after increasing by three times over the past ten years.

- There is still opportunity for considerable growth in China's healthcare market, with per capita healthcare spending at just over $350, compared to an average of $4,986 among the Organization for Economic Cooperation and Development (OECD) countries.

- China's aging population, rising incomes, and increasing urbanization may provide a sustained catalyst for growth in China's healthcare sector.

KURE features:

- Exposure to Chinese companies listed in Mainland China, Hong Kong, and the United States that are involved in the healthcare industry.

- Exposure to key healthcare subsectors: Biotechnology, General Pharmaceuticals, Care Providers, Medical Devices, and Traditional Chinese Medicine.

- Exposure to companies that may benefit from China's growing middle class and aging population.

- Access to major global healthcare companies that are often not captured by broad indexes.

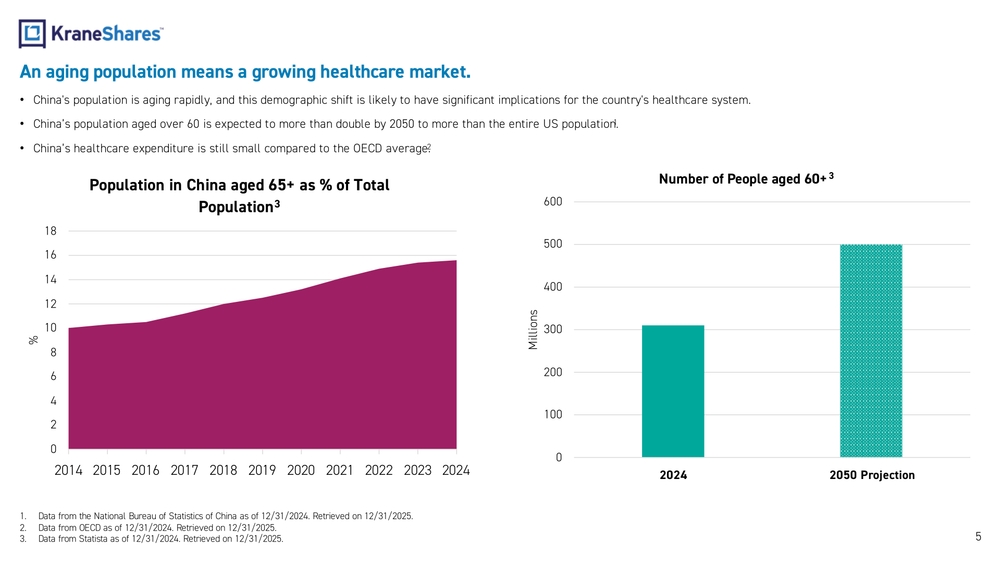

An aging population means a growing healthcare market.

- China's population is aging rapidly, and this demographic shift is likely to have significant implications for the country's healthcare system.

- China's population aged over 60 is expected to more than double by 2050 to more than the entire US population.

- China's healthcare expenditure is still small compared to the OECD average.

Population in China aged 65+ as % of Total Population

Chart showing increasing trend from 2014 to 2024, rising from approximately 10% to 15%

Number of People aged 60+

Chart comparing 2024 (approximately 300 million) to 2050 Projection (approximately 500 million)

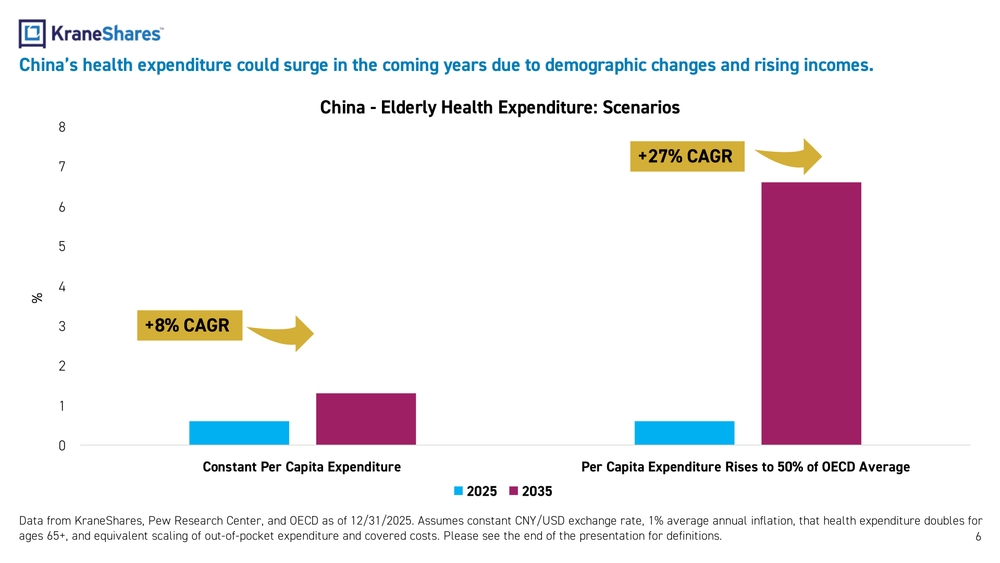

China's health expenditure could surge in the coming years due to demographic changes and rising incomes.

China - Elderly Health Expenditure: Scenarios

Chart showing two scenarios:

- Constant Per Capita Expenditure: Shows growth from 2025 to 2035 with +8% CAGR

- Per Capita Expenditure Rises to 50% of OECD Average: Shows much higher growth with +27% CAGR

Data from KraneShares, Pew Research Center, and OECD as of 12/31/2025. Assumes constant CNY/USD exchange rate, 1% average annual inflation, that health expenditure doubles for ages 65+, and equivalent scaling of out-of-pocket expenditure and covered costs.

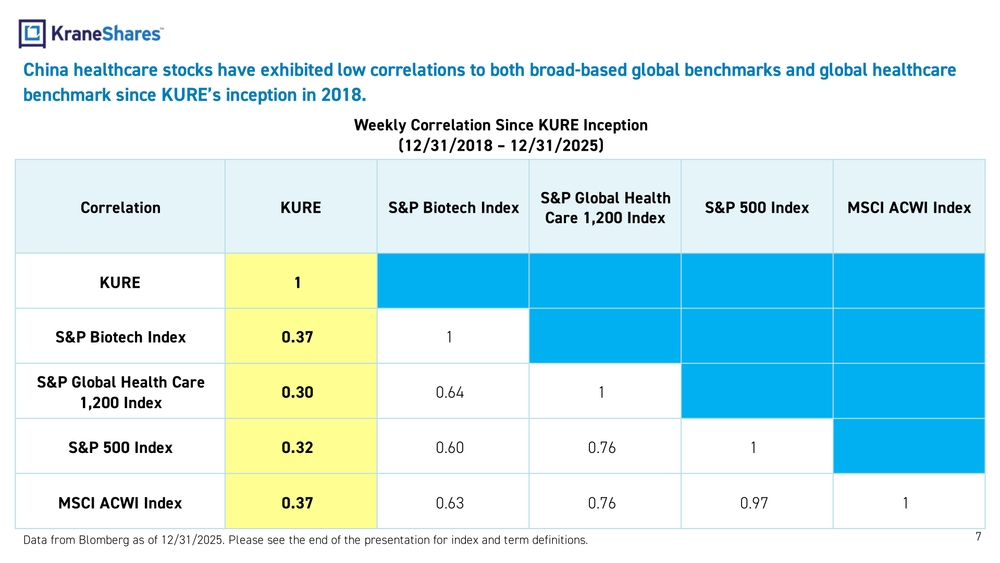

China healthcare stocks have exhibited low correlations to both broad-based global benchmarks and global healthcare benchmark since KURE's inception in 2018.

Weekly Correlation Since KURE Inception (12/31/2018 – 12/31/2025)

| Correlation | KURE | S&P Biotech Index | S&P Global Health Care 1,200 Index | S&P 500 Index | MSCI ACWI Index |

|---|---|---|---|---|---|

| KURE | 1 | ||||

| S&P Biotech Index | 0.37 | 1 | |||

| S&P Global Health Care 1,200 Index | 0.30 | 0.64 | 1 | ||

| S&P 500 Index | 0.32 | 0.60 | 0.76 | 1 | |

| MSCI ACWI Index | 0.37 | 0.63 | 0.76 | 0.97 | 1 |

Data from Bloomberg as of 12/31/2025.

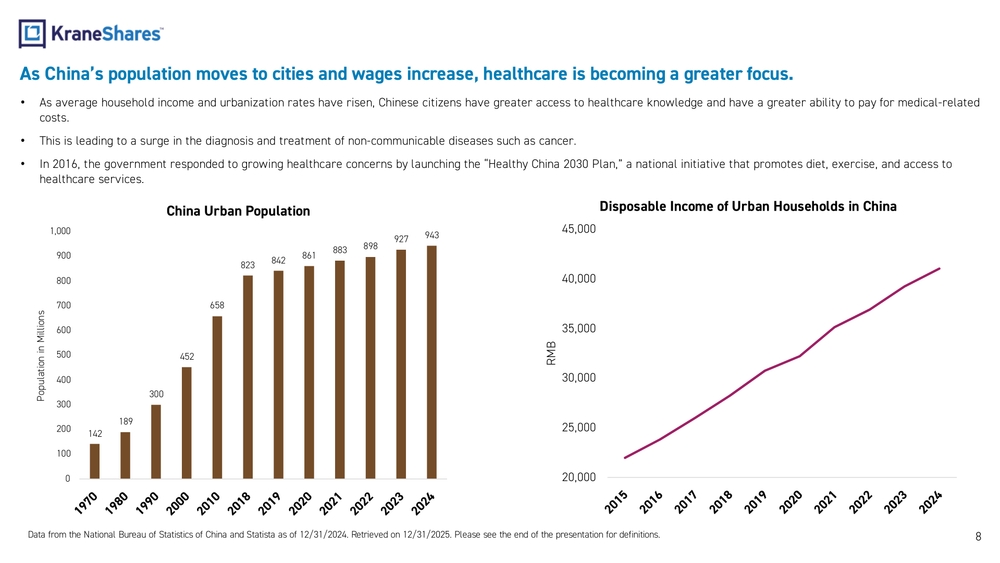

As China's population moves to cities and wages increase, healthcare is becoming a greater focus.

- As average household income and urbanization rates have risen, Chinese citizens have greater access to healthcare knowledge and have a greater ability to pay for medical-related costs.

- This is leading to a surge in the diagnosis and treatment of non-communicable diseases such as cancer.

- In 2016, the government responded to growing healthcare concerns by launching the "Healthy China 2030 Plan," a national initiative that promotes diet, exercise, and access to healthcare services.

China Urban Population

Chart showing growth in urban population from 1970 (142 million) to 2024 (943 million)

Disposable Income of Urban Households in China

Chart showing rising trend of disposable income from 2015 to 2024

Data from the National Bureau of Statistics of China and Statista as of 12/31/2024.

China's domestic pharmaceutical market could be poised for significant future growth after regulatory overhaul.

- China's pharmaceutical sales are estimated to have been approximately $120 billion in 2025 and maintain a compound annual growth rate (CAGR) of 7.22% through 2028.

- Per capita, out-of-pocket health spending remains low at $350, as compared to an average of around $5,000 for OECD countries, implying significant upside potential for health spending.

- Thanks to universal single-payer health insurance established in 2011, 95% of China's population has access to health care services.

China Total Annual Pharmaceutical Sales

Chart showing pharmaceutical sales trends from 2012 to 2025, with annotations for:

- Launch of "Healthy China 2030 Plan"

- The expansion of the scope of centralized drug and device approvals and purchasing led to a sales slump in the short term.

- Sales return to growth.

Data from Statista, Trivium China, OECD, World Bank, KraneShares as of 12/31/2025.

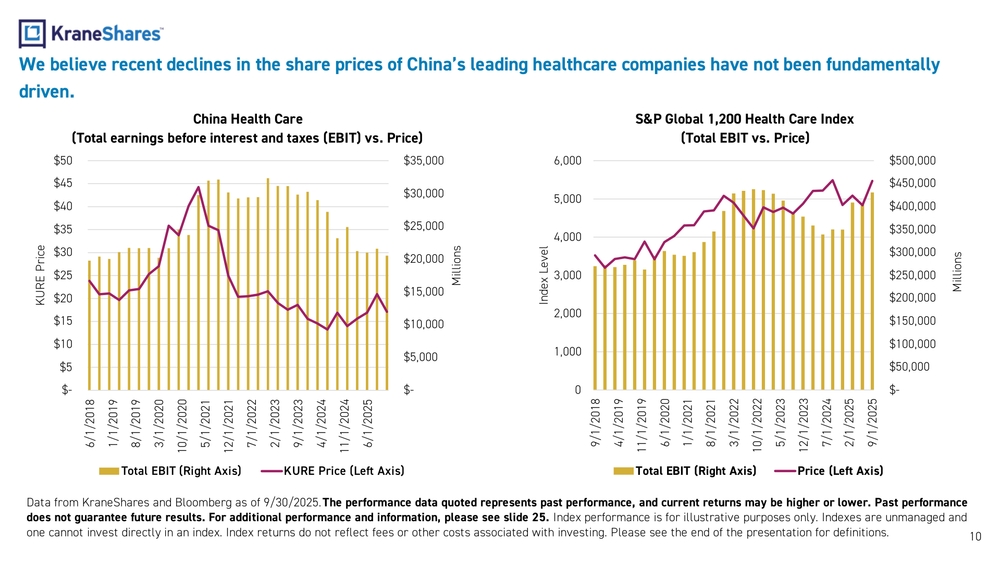

We believe recent declines in the share prices of China's leading healthcare companies have not been fundamentally driven.

China Health Care (Total earnings before interest and taxes (EBIT) vs. Price)

Chart comparing KURE Price (left axis) with Total EBIT (right axis) from 2018 to 2025, showing price declines despite relatively stable or growing EBIT

S&P Global 1,200 Health Care Index (Total EBIT vs. Price)

Chart comparing Price (left axis) with Total EBIT (right axis) from 2018 to 2025, showing more correlation between price and EBIT

Data from KraneShares and Bloomberg as of 9/30/2025. The performance data quoted represents past performance, and current returns may be higher or lower. Past performance does not guarantee future results.

China's Healthcare Ecosystem

- General Pharmaceuticals

- Medical Devices

- Care Providers

- Biotechnology

- Traditional Chinese Medicine

Contract Research Organizations (CRO) Overview

- CROs use their state-of-the-art, turn-key labs with advanced technological capabilities and access to a deep bench of scientists to develop new drugs and treatments for companies that wish to outsource their R&D processes.

- They are thereby able to profit from the global R&D process without bearing as much risk, which makes for a defensive business model.

- Industry leaders Wuxi Biologics and Wuxi Apptec provide end-to-end support to pharmaceuticals from discovery to commercialization.

Main Beneficiaries of Research and Development (R&D) Spending

- Contract organizations are the main beneficiaries of the strong growth in R&D spending in China as more companies outsource their R&D needs.

- Contract research organizations also receive R&D spending from abroad as multinationals hire them to test and develop new drugs.

Innovations

- Akeso has developed a new lung cancer treatment that could be twice as effective as the current global best-in-class treatments, based on clinical trial data.

Biotechnology

- WuXi AppTec is a global tech platform that offers a portfolio of medical R&D resources to shorten the lag time in biomedical discovery and innovative development.

Contract Research Organizations

- WuXi Biologics is a leading global contract research, development, and marketing (CRDMO) offering end-to-end solutions that enable partners to discover, develop, and manufacture biologics.

- Innovent Biologics is committed to developing, manufacturing, and commercializing high quality, innovative medicines for the treatment of major diseases such as cancer.

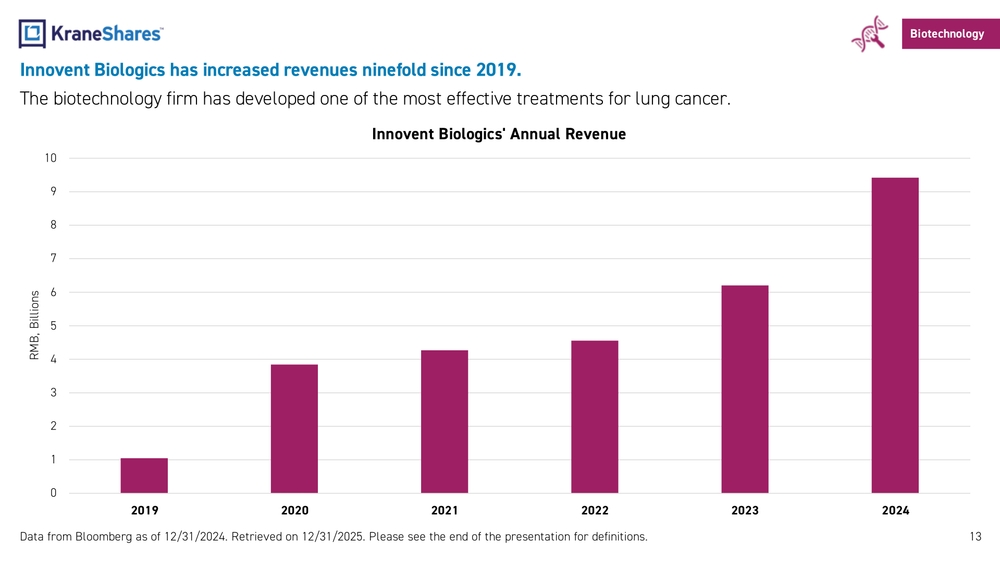

Innovent Biologics has increased revenues ninefold since 2019.

The biotechnology firm has developed one of the most effective treatments for lung cancer.

Innovent Biologics' Annual Revenue

[Chart showing revenue growth from 2019 to 2024, with values in RMB, Billions: 2019: ~1 billion 2020: ~4 billion 2021: ~4.2 billion 2022: ~4.6 billion 2023: ~6.2 billion 2024: ~9.5 billion]

Out-Licensing and In-Licensing represent a significant opportunity for China's pharmaceutical firms.

Definitions:

- Out-Licensing: The practice of selling pharmaceuticals or medical devices developed in China in international markets.

- In-Licensing: The practice of selling pharmaceuticals or medical devices developed in international markets in China.

Favorable Policies

Several market-friendly policies have been introduced encouraging joint ventures between multinational companies and domestic companies, which include:

- Increasing efficiency and transparency of drug review and approval processes

- Maximizing quality of generic drugs

- Enhancing efficiency in R&D innovations

- The Chinese government has been working to speed up the approval process for new drugs and to encourage the development of innovative drugs in recent years.

Pharmaceutical In-Licensing

The Hisun-Pfizer joint venture is mutually beneficial in international marketing and in the commercialization of generic medicines in China.

Medial Devices In-Licensing

Fosun Pharma and Intuitive Surgical's joint venture is mutually beneficial in biomedical technology and pharmaceutical manufacturing and distribution.

Pharmaceutical Out-Licensing

Eli Lilly developed a lung cancer treatment with Innovent.

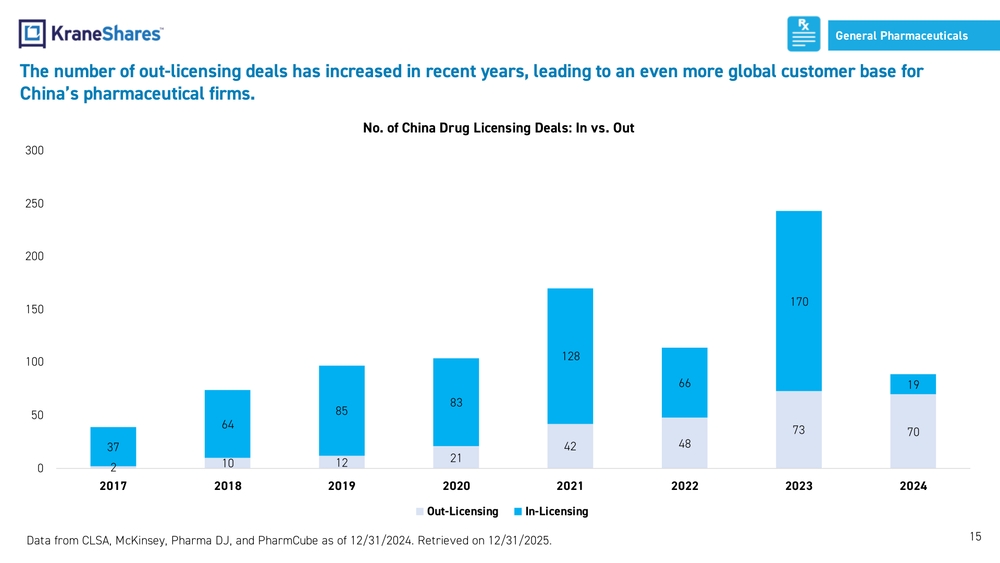

The number of out-licensing deals has increased in recent years, leading to an even more global customer base for China's pharmaceutical firms.

No. of China Drug Licensing Deals: In vs. Out

[Chart showing the number of In-Licensing and Out-Licensing deals from 2017 to 2024:

2017: 2 Out-Licensing, 37 In-Licensing 2018: 10 Out-Licensing, 64 In-Licensing 2019: 12 Out-Licensing, 85 In-Licensing 2020: 21 Out-Licensing, 83 In-Licensing 2021: 42 Out-Licensing, 128 In-Licensing 2022: 48 Out-Licensing, 66 In-Licensing 2023: 73 Out-Licensing, 170 In-Licensing 2024: 70 Out-Licensing, 19 In-Licensing]

China's medical device market is world-class with both domestic and international customer bases.

-

Due to perceived quality advantages, medical equipment imports from the U.S. and Europe remain high. However, as quality increases, Chinese domestic medical device companies are increasingly competing with U.S. and European companies, making particularly strong gains in medium-level technology niches.

-

In addition to benefitting from strong domestic demand, China's top medical device companies have overseas operations and serve customers globally.

China Medical Devices Market

| Metric | Value |

|---|---|

| Total Market Size ($ Billions) | 45.0 |

| Expected Compound Annual Growth Rate (CAGR) 2025-2032 (%) | 9.40% |

Medical Devices

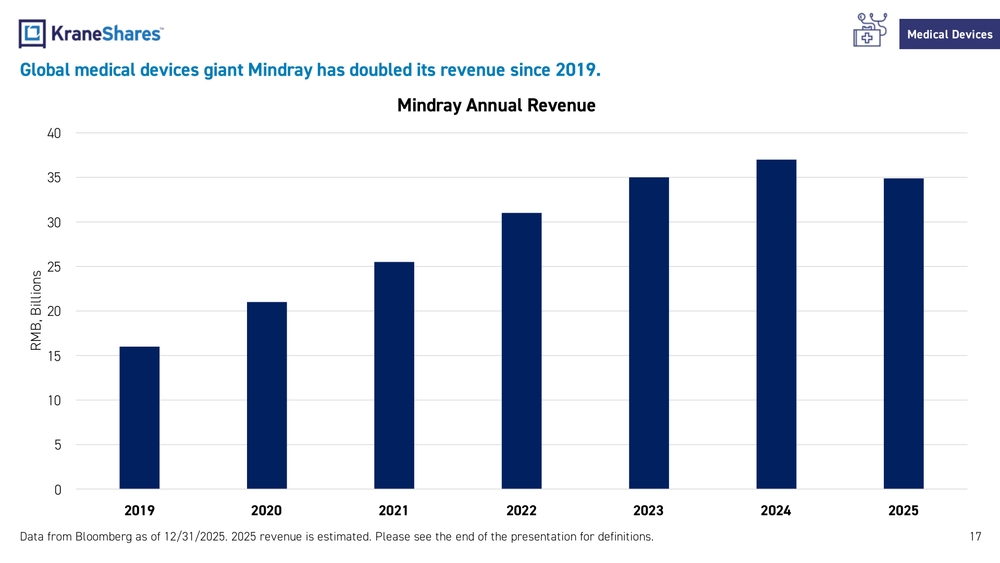

Mindray is a leading global supplier of in-vitro fertilization equipment, ventilators, among other key medical devices.

Global medical devices giant Mindray has doubled its revenue since 2019.

Mindray Annual Revenue

[Chart showing revenue growth from 2019 to 2025, with values in RMB, Billions: 2019: ~16 billion 2020: ~21 billion 2021: ~25 billion 2022: ~31 billion 2023: ~35 billion 2024: ~37 billion 2025: ~35 billion (estimated)]

The Traditional Chinese Medicine (TCM) industry represents a sizable portion of the entire market.

-

TCM has a rich 2,000-year history encompassing herbal medicine, acupuncture, massage and dietetics.

-

In December 2016, China's State Council issued the "Strategic Plan on the Development of Traditional Chinese Medicine," making the development of TCM a national strategy. The policy emphasizes promoting a balance between Western medicine and TCM practices.

-

TCM has a global footprint, and the global TCM market was valued at $86 billion in 2025 and is expected to grow to $98 billion by 2032.

-

TCM practitioners emphasize preventative medicine and treating diseases before they occur through healthy living and proper diets. This is especially important in China, which has increased obesity, diabetes, and smoking rates.

-

TCM companies can also benefit from increasing incomes and consumer spending, as many TCM products are popular for personal wellness purposes rather than urgent medical needs.

TCM has over 2,000 years of tradition

In Traditional Chinese Medicine, good health is believed to be achieved by a balance between yin and yang.

Traditional Chinese Medicine

Tong Ren Tang manufactures and sells traditional remedies in China and abroad.

As China's population becomes more health conscious, the demand for high quality preventative care also increases, providing a catalyst for private hospitals and facilities that offer health examinations, evaluations, and consulting services.

Privatization

-

Rising demand from wealthier Chinese seeking quality care and diverse services has led to increased privatization of hospitals to match demand, but public hospitals still far outnumber private hospitals.

-

We believe China's public hospital system will be insufficient to satisfy the need of the population through 2050, leading to the establishment of more private hospitals.

Healthy China 2030: Upgrading Primary Care Institutions

-

The "Healthy China 2030" policy outlines the government's plans to upgrade the standards and quality of service in primary care institutions.

-

The government sees general practitioners as the gatekeepers of people's health and primary method of controlling medical expenditures.

-

By 2030, the goal is to have five qualified general practitioners available for every 10,000 residents in China.

-

The National Health and Family Planning Commission estimates China needs to add 210,000 general practitioners.

-

The establishment of a medical network and referral system may help reduce overcrowding in China's largest tertiary hospitals.

Care Provider

Aier Eye Hospital is a leading private hospital administrator in China and globally. Aier operates 718 ophthalmology facilities in Mainland China, 101 clinics in Europe, 8 clinics in Hong Kong, 14 clinics in Southeast Asia, and one clinic in the United States.

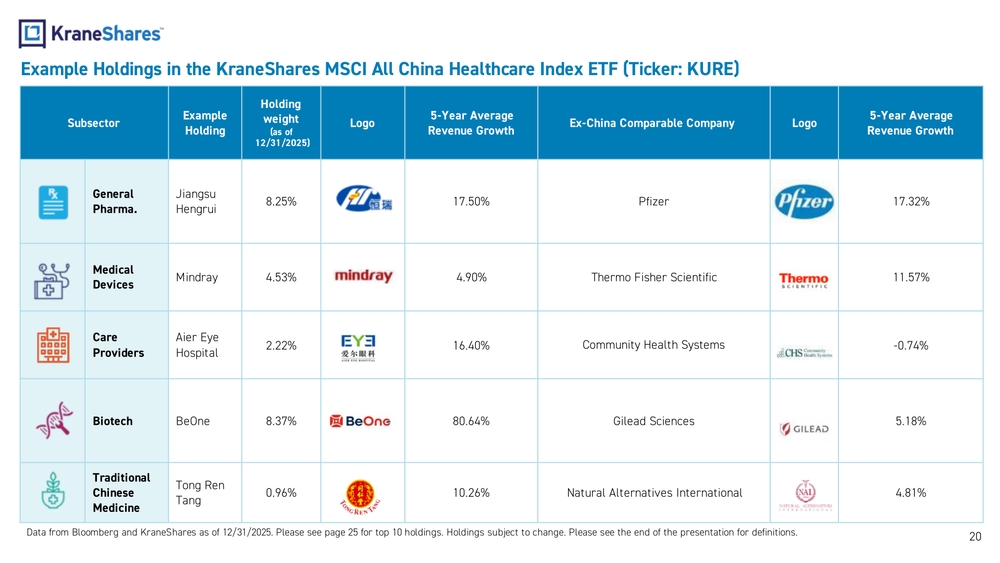

Example Holdings in the KraneShares MSCI All China Healthcare Index ETF (Ticker: KURE)

| Subsector | Example Holding | Holding weight (as of 12/31/2025) | 5-Year Average Revenue Growth | Ex-China Comparable Company | 5-Year Average Revenue Growth |

|---|---|---|---|---|---|

| General Pharma. | Jiangsu Hengrui | 8.25% | 17.50% | Pfizer | 17.32% |

| Medical Devices | Mindray | 4.53% | 4.90% | Thermo Fisher Scientific | 11.57% |

| Care Providers | Aier Eye Hospital | 2.22% | 16.40% | Community Health Systems | -0.74% |

| Biotech | BeOne | 8.37% | 80.64% | Gilead Sciences | 5.18% |

| Traditional Chinese Medicine | Tong Ren Tang | 0.96% | 10.26% | Natural Alternatives International | 4.81% |

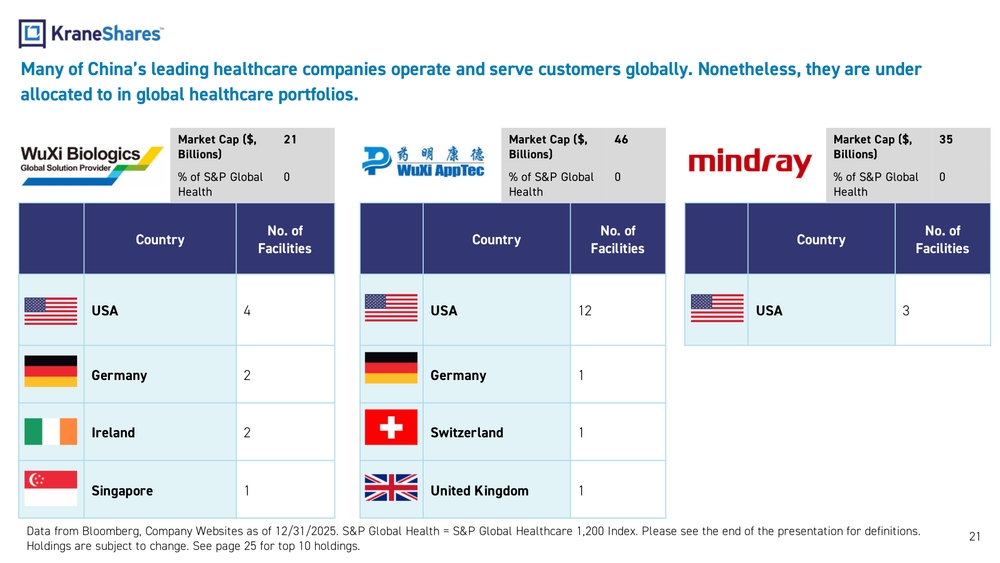

Many of China's leading healthcare companies operate and serve customers globally. Nonetheless, they are under allocated to in global healthcare portfolios.

| Company | Market Cap ($, Billions) | % of S&P Global Health | Country | No. of Facilities |

|---|---|---|---|---|

| WuXi Biologics | 21 | 0 | USA | 4 |

| Germany | 2 | |||

| Ireland | 2 | |||

| Singapore | 1 | |||

| WuXi AppTec | 46 | 0 | USA | 12 |

| Germany | 1 | |||

| Switzerland | 1 | |||

| United Kingdom | 1 | |||

| Mindray | 35 | 0 | USA | 3 |

Data from Bloomberg, Company Websites as of 12/31/2025. S&P Global Health = S&P Global Healthcare 1,200 Index. Please see the end of the presentation for definitions. Holdings are subject to change. See page 25 for top 10 holdings.

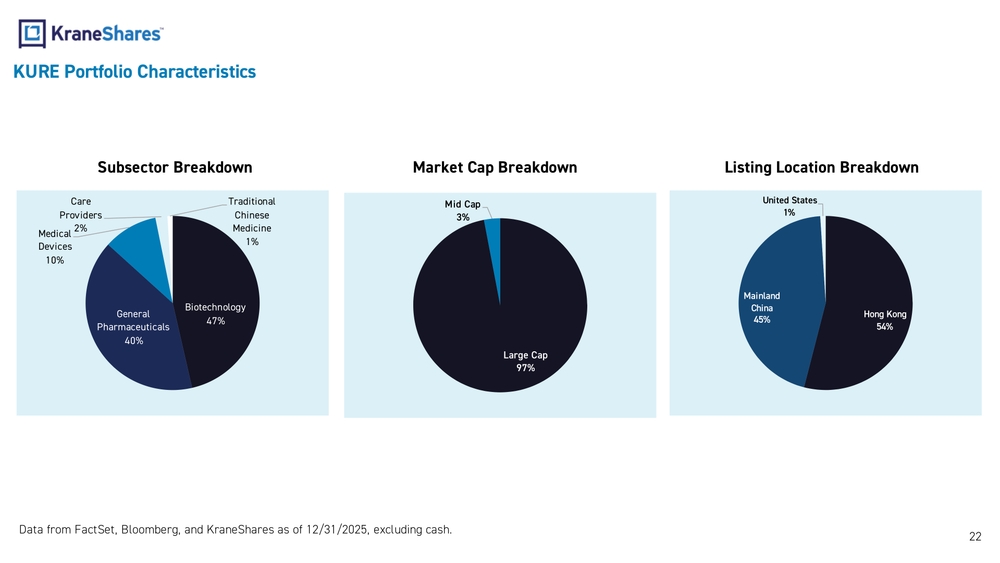

KURE Portfolio Characteristics

Subsector Breakdown

- Biotechnology: 47%

- General Pharmaceuticals: 40%

- Medical Devices: 10%

- Care Providers: 2%

- Traditional Chinese Medicine: 1%

Market Cap Breakdown

- Large Cap: 97%

- Mid Cap: 3%

Listing Location Breakdown

- Hong Kong: 54%

- Mainland China: 45%

- United States: 1%

Data from FactSet, Bloomberg, and KraneShares as of 12/31/2025, excluding cash.

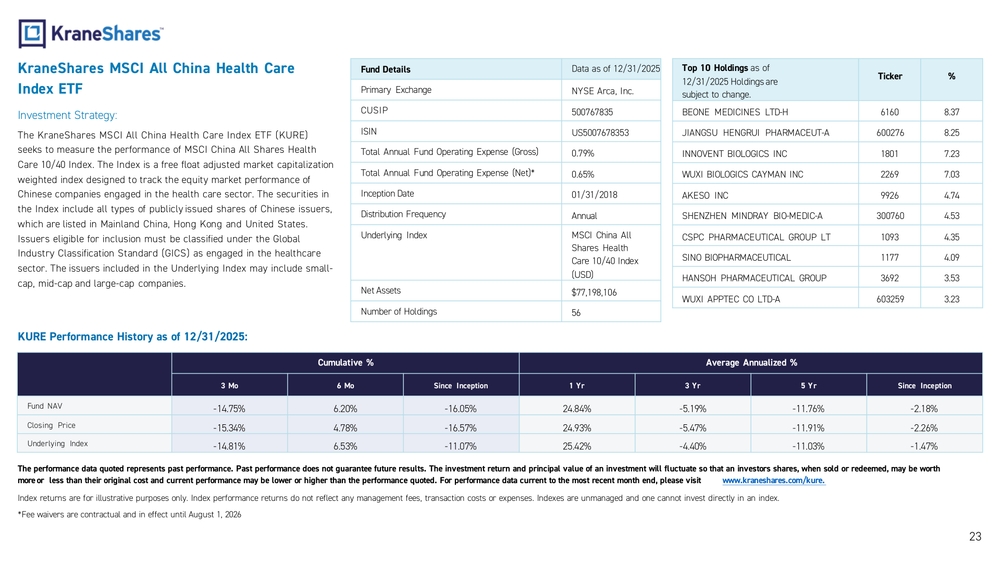

KraneShares MSCI All China Health Care Index ETF

Investment Strategy:

The KraneShares MSCI All China Health Care Index ETF (KURE) seeks to measure the performance of MSCI China All Shares Health Care 10/40 Index. The Index is a free float adjusted market capitalization weighted index designed to track the equity market performance of Chinese companies engaged in the health care sector. The securities in the Index include all types of publicly issued shares of Chinese issuers, which are listed in Mainland China, Hong Kong and United States. Issuers eligible for inclusion must be classified under the Global Industry Classification Standard (GICS) as engaged in the healthcare sector. The issuers included in the Underlying Index may include small-cap, mid-cap and large-cap companies.

Fund Details Data as of 12/31/2025

- Primary Exchange: NYSE Arca, Inc.

- CUSIP: 500767835

- ISIN: US5007678353

- Total Annual Fund Operating Expense (Gross): 0.79%

- Total Annual Fund Operating Expense (Net)*: 0.65%

- Inception Date: 01/31/2018

- Distribution Frequency: Annual

- Underlying Index: MSCI China All Shares Health Care 10/40 Index (USD)

- Net Assets: $77,198,106

- Number of Holdings: 56

Top 10 Holdings as of 12/31/2025 Holdings are subject to change.

| Company | Ticker | % |

|---|---|---|

| BEONE MEDICINES LTD-H | 6160 | 8.37 |

| JIANGSU HENGRUI PHARMACEUT-A | 600276 | 8.25 |

| INNOVENT BIOLOGICS INC | 1801 | 7.23 |

| WUXI BIOLOGICS CAYMAN INC | 2269 | 7.03 |

| AKESO INC | 9926 | 4.74 |

| SHENZHEN MINDRAY BIO-MEDIC-A | 300760 | 4.53 |

| CSPC PHARMACEUTICAL GROUP LT | 1093 | 4.35 |

| SINO BIOPHARMACEUTICAL | 1177 | 4.09 |

| HANSOH PHARMACEUTICAL GROUP | 3692 | 3.53 |

| WUXI APPTEC CO LTD-A | 603259 | 3.23 |

KURE Performance History as of 12/31/2025:

Cumulative %

| 3 Mo | 6 Mo | Since Inception | |

|---|---|---|---|

| Fund NAV | -14.75% | 6.20% | -16.05% |

| Closing Price | -15.34% | 4.78% | -16.57% |

| Underlying Index | -14.81% | 6.53% | -11.07% |

Average Annualized %

| 1 Yr | 3 Yr | 5 Yr | Since Inception | |

|---|---|---|---|---|

| Fund NAV | 24.84% | -5.19% | -11.76% | -2.18% |

| Closing Price | 24.93% | -5.47% | -11.91% | -2.26% |

| Underlying Index | 25.42% | -4.40% | -11.03% | -1.47% |

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investors shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please visit www.kraneshares.com/kure.

Index returns are for illustrative purposes only. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

*Fee waivers are contractual and in effect until August 1, 2026

Index Definitions:

S&P Global 1,200 Health Care Index: The S&P Global 1,200 Health Care index consists of all members of the S&P Global 1,200 that are classified within the GICS® health care sector, including both developed and emerging markets. The index was launched on September 30, 1999.

MSCI World Health Care Index: The MSCI World Health Care Index is designed to capture the large and mid cap segments across 23 Developed Markets (DM) countries*. All securities in the index are classified in the Health Care as per the Global Industry Classification Standard (GICS®). The index was launched on September 15, 1999.

S&P Biotech Index: S&P Select Industry indexes are designed to measure the performance of narrow GICS sub-industries. The S&P Biotechnology Select Industry Index comprises stocks in the S&P Total Market Index that are classified in the GICS Biotechnology sub-industry. The index was launched on January 27, 2006.

S&P 500 Index: The S&P 500 Index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 9.9 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 3.4 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization. The index was launched on March 4, 1957.

MSCI All Country World Index (ACWI): The MSCI ACWI captures large and mid-cap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries*. With 2,558 constituents, the index covers approximately 85% of the global investable equity opportunity set. The index was launched on May 31, 1990.

Term Definitions:

Earnings before Interest and Taxes (EBIT): A company's total revenue before deducting interest and taxes.

Price to Earnings Ratio (P/E): A company's share price divided by its earnings per share. The P/E ratio is meant to provide a sense of whether a company is over or under-valued.

Revenue: The money a company makes from selling goods and services, before the deduction of any expenses.

Revenue Growth: The change in a company's revenues over a specified period of time.

Compound Annual Growth Rate (CAGR): The compound annual growth rate is the rate of return would be required for an investment to grow from its beginning balance to its ending balance, assuming the profits were reinvested at the end of each period of the investment's life span.

Urban Population: Population of urban and suburban areas.

Disposable Income: The income that does not go towards housing and basic necessities.

Per Capita Expenditure: The average annual spending per person on healthcare needs, including both out-of-pocket costs and covered expenses.

Correlation: The degree to which two variables, in this case investments, move in tandem with one another. It is expressed using a number between -1 and 1, with -1 indicating a perfectly inverse relationship, 0 indicating no synchronization whatsoever, and 1 indicating they always move in lockstep with one another.

Important Notes:

Carefully consider the Funds' investment objectives, risk factors, charges and expenses before investing. This and additional information can be found in the Funds' full and summary prospectus, which may be obtained by visiting www.kraneshares.com/kure/ Read the prospectus carefully before investing.

Risk Disclosures:

Investing involves risk, including possible loss of principal. There can be no assurance that a Fund will achieve its stated objectives. Indices are unmanaged and do not include the effect of fees. One cannot invest directly in an index.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change. Certain content represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results; material is as of the dates noted and is subject to change without notice.

The Fund may invest in derivatives, which are often more volatile than other investments and may magnify the Fund's gains or losses. A derivative (i.e., futures/forward contracts, swaps, and options) is a contract that derives its value from the performance of an underlying asset. The primary risk of derivatives is that changes in the asset's market value and the derivative may not be proportionate, and some derivatives can have the potential for unlimited losses. Derivatives are also subject to liquidity and counterparty risk. The Fund is subject to liquidity risk, meaning that certain investments may become difficult to purchase or sell at a reasonable time and price. If a transaction for these securities is large, it may not be possible to initiate, which may cause the Fund to suffer losses. Counterparty risk is the risk of loss in the event that the counterparty to an agreement fails to make required payments or otherwise comply with the terms of the derivative.

The ability of the Fund to achieve its respective investment objectives is dependent, in part, on the continuous availability of A Shares and the ability to obtain, if necessary, additional A Shares quota. If the Fund is unable to obtain sufficient exposure to limited availability of A Share quota, the Fund could seek exposure to the component securities of the Underlying Index by investment in other types of securities. The Fund is subject to political, social or economic instability within China which may cause decline in value. Emerging markets involve heightened risk related to the same factors as well as increase volatility and lower trading volume. Fluctuations in currency of foreign countries may have an adverse effect to domestic currency values. The Fund may invest in Initial Public Offerings (IPOs). Securities issued in IPOs have no trading history, and information about the companies may be available for very limited periods. In addition, the prices of securities sold in IPOs may be highly volatile. In addition, as the Fund increases in size, the impact of IPOs on the Fund's performance will generally decrease.

Narrowly focused investments typically exhibit higher volatility. The Fund's assets are expected to be concentrated in a sector, industry, market, or group of concentrations to the extent that the Underlying Index has such concentrations. The securities or futures in that concentration could react similarly to market developments. Thus, the Fund is subject to loss due to adverse occurrences that affect that concentration. In addition to the normal risks associated with investing, investments in smaller companies typically exhibit higher volatility. KURE is non-diversified.

ETF shares are bought and sold on an exchange at market price (not NAV) and are not individually redeemed from the Fund. However, shares may be redeemed at NAV directly by certain authorized broker-dealers (Authorized Participants) in very large creation/redemption units. The returns shown do not represent the returns you would receive if you traded shares at other times. Shares may trade at a premium or discount to their NAV in the secondary market. Brokerage commissions will reduce returns. Beginning 12/23/2020, market price returns are based on the official closing price of an ETF share or, if the official closing price isn't available, the midpoint between the national best bid and national best offer ("NBBO") as of the time the ETF calculates the current NAV per share. Prior to that date, market price returns were based on the midpoint between the Bid and Ask price. NAVs are calculated using prices as of 4:00 PM Eastern Time.

The KraneShares ETFs and KFA Funds ETFs are distributed by SEI Investments Distribution Company (SIDCO), 1 Freedom Valley Drive, Oaks, PA 19456, which is not affiliated with Krane Funds Advisors, LLC, the Investment Adviser for the Funds, or any sub-advisers for the Funds.